A few weeks back, I looked at Singtel stock and concluded that I actually really liked what I saw. The transformation of Singtel looked promising, and the charts looked phenomenal. Along that line of reasoning. There’s another TLC that I’ve been monitoring for a while, and that I wanted to do a deep dive into. Keppel. What […]

The post Why I may buy Keppel stock at 5.0% dividend yield? Infrastructure play well positioned for the next decade? appeared first on Financial Horse.

A few weeks back, I looked at Singtel stock and concluded that I actually really liked what I saw.

The transformation of Singtel looked promising, and the charts looked phenomenal.

Along that line of reasoning.

There’s another TLC that I’ve been monitoring for a while, and that I wanted to do a deep dive into.

Keppel.

To give credit where credit is due.

I do think (like Singtel), Keppel’s management done well in restructuring the company.

The slides below set this out.

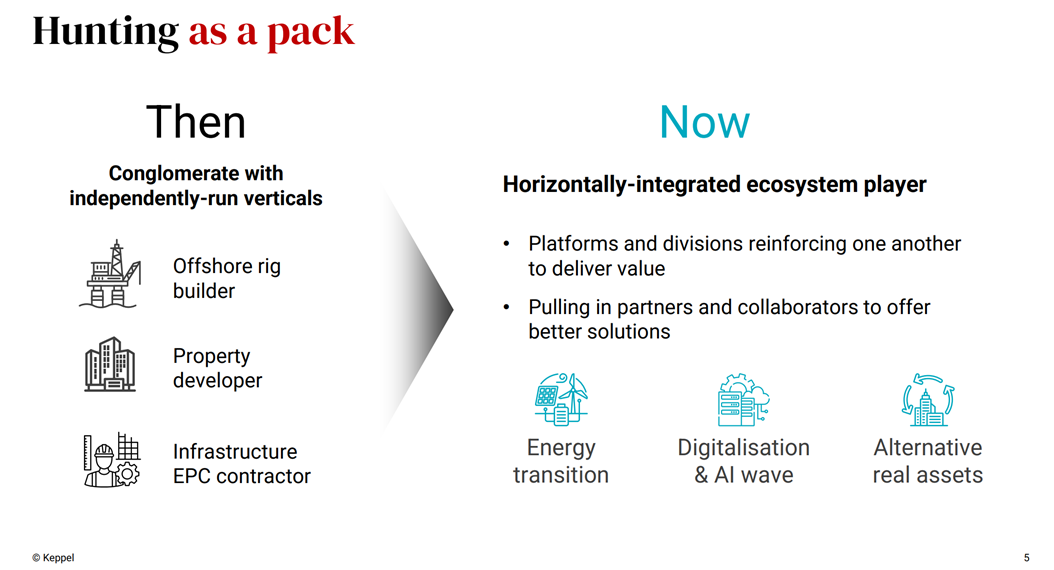

A key one was the divestment of the lossmaking Keppel Offshore & Marine – which took a huge liability off the books of Keppel, paving the way for the subsequent transformation.

This was followed by the restructuring of Keppel into 3 distinct platforms / ecosystems:

- Energy

- Real Estate

- Digitisation / AI

Energy is basically today’s infrastructure segment, while digitisation / AI is connectivity.

In terms of profit split, you can see how the biggest profit maker by far is infrastructure, followed by real estate,

With connectivity coming in a distant last.

Share price was phenomenal during the 2022 period due to inflationary pressures from the Ukraine war (higher electricity prices).

Share price rallied almost 100% from $3.5 to $7 during this period.

Since 2023 however, you can see how the share price has been pretty much rangebound for 2 years.

So charts wise I would say Keppel doesn’t look as attractive as Singtel, but let’s take a closer look at the fundamentals before we jump to any conclusions.

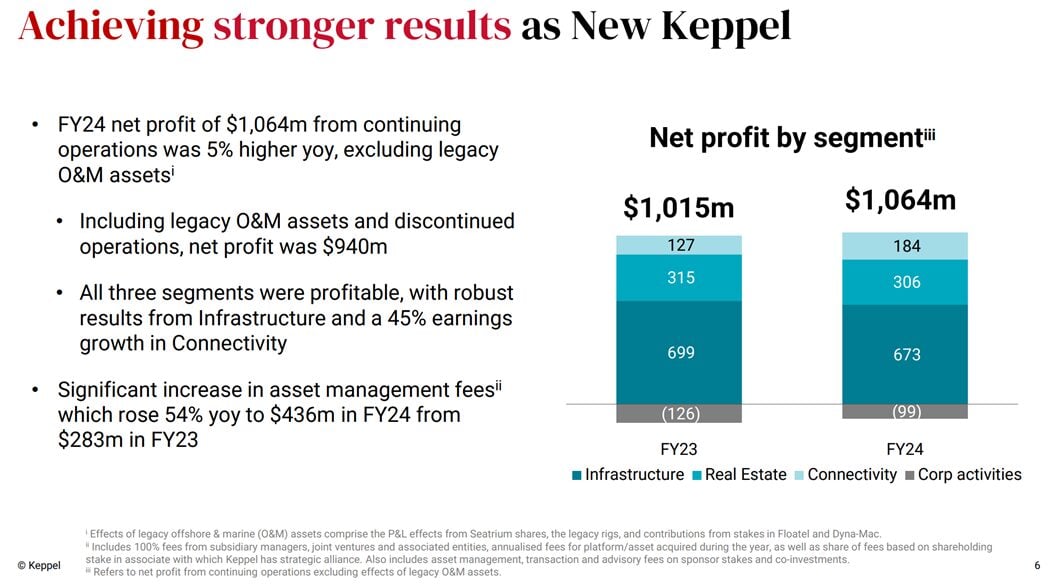

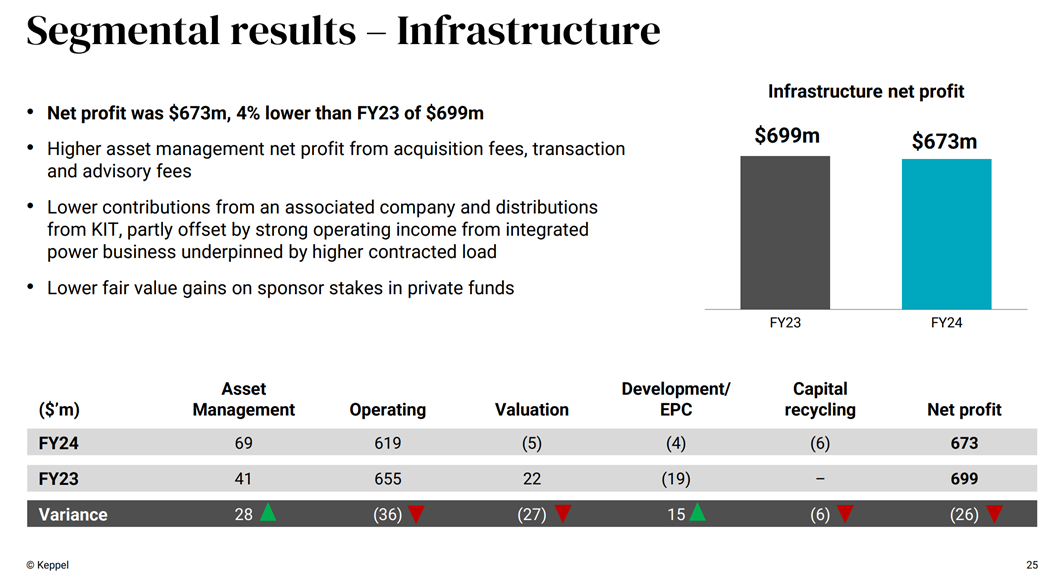

The bulk of Keppel’s profits today (67%) comes from infrastructure (energy).

And you know what – I actually think this is a good thing, because infrastructure in today’s more inflationary, deglobalized world, is actually a pretty under tapped asset class.

You can see how a lot of the smart money like Blackrock is trying to build their exposure to infrastructure assets going forward.

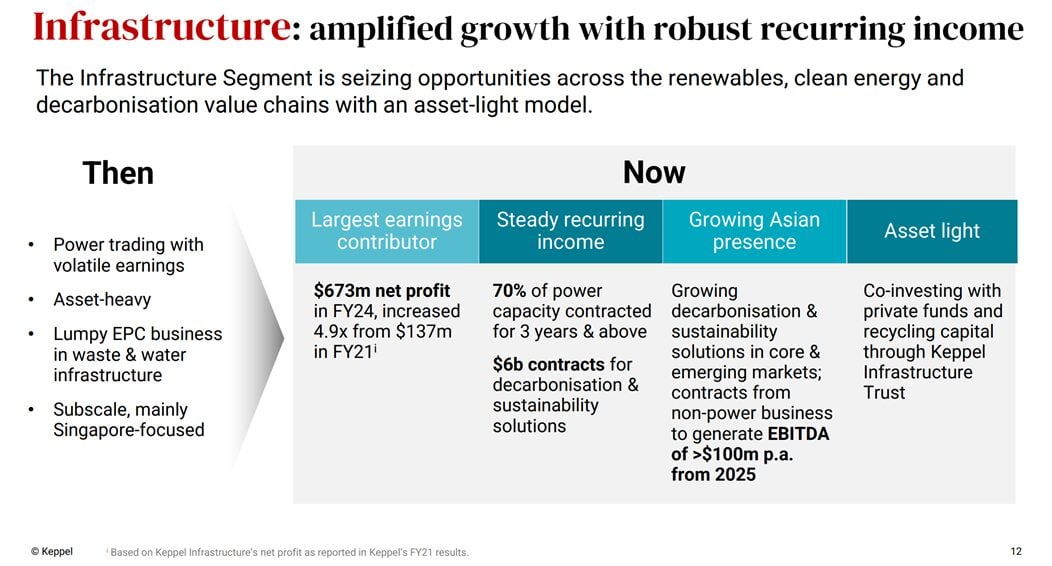

You might ask what exactly is infrastructure, especially given that this is Keppel’s largest profit maker?

While it used to be a mix of energy generation, waste and water infrastructure and so on, the bulk of it is basically electricity generation today.

In Singapore at least, this is a good and fairly stable business, as the supply (and demand) is tightly controlled by the government, so you don’t need to worry about oversupply issues.

Of course on the flipside, you could argue that this means that short of an exceptional event like COVID / Ukraine war, there isn’t the potential for massive upside in electricity prices.

And I suppose that’s a fair point too – which is why you see Keppel’s share price rangebound for 2 years despite the exceptional profits they are making.

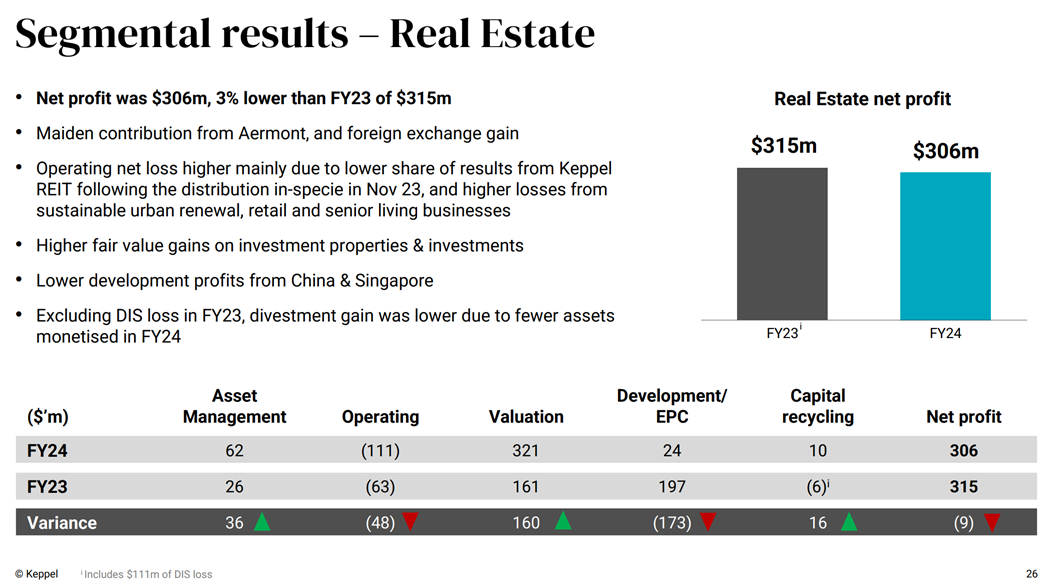

The second largest profit maker – is real estate.

And boy… real estate today, is no longer real estate of the past 20 years.

When Singapore was still growing strongly in the 2000s, and when interest rates were stuck at zero in the 2010s, real estate was king.

But in today’s world, with structurally higher inflation and interest rates, and an era of deglobalisation – Real Estate is just not what it used to be any more.

The structural tailwinds are no longer there.

Which is why you can see how Keppel described their real estate strategy as “prioritising the growth of recurring income through asset-light real estate solutions”.

And this might be me being cynical – but I read that as basically saying they no longer want to take big positions in real estate, and they want to manage real estate instead (asset light).

In terms of execution, you can see how the balance sheet has shrunk from $15.7 billion in 2017 to $14.1 billion in 2024.

While the value of their China land bank has shrunk from $3.1 billion to $1.1 billion.

And you know what – I agree with this strategy.

Real estate doesn’t have the same structural tailwinds this decade.

If you want to improve ROE, you need to be asset light.

Offload the big real estate positions into a REIT / Fund vehicle (to investors who want that exposure), and focus on earning the management fees instead.

Ie – Asset light, recurring income.

Buzzwords that investors love.

But at the end of the day.

My view – there’s just so much you can do with real estate in this market, given that the structural tailwinds of zero interest rates or strong economic growth are no longer in place.

It goes back to that Buffett quote about “When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

Real estate is still generating good profits so they can’t get rid of it, but in my mind the future will lie with the infrastructure and connectivity parts of Keppel’s business.

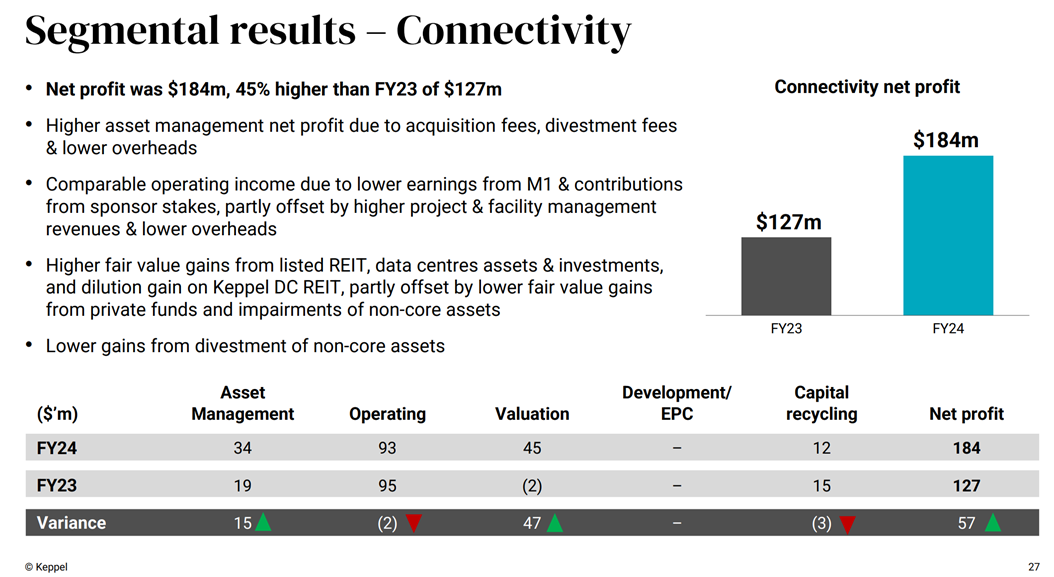

The final sector is connectivity.

And you can see that while infrastructure and real estate profit growth has been flat.

Connectivity has seen a massive 57% growth in profits.

So for now at least – connectivity is the growth sector.

And what exactly is connectivity?

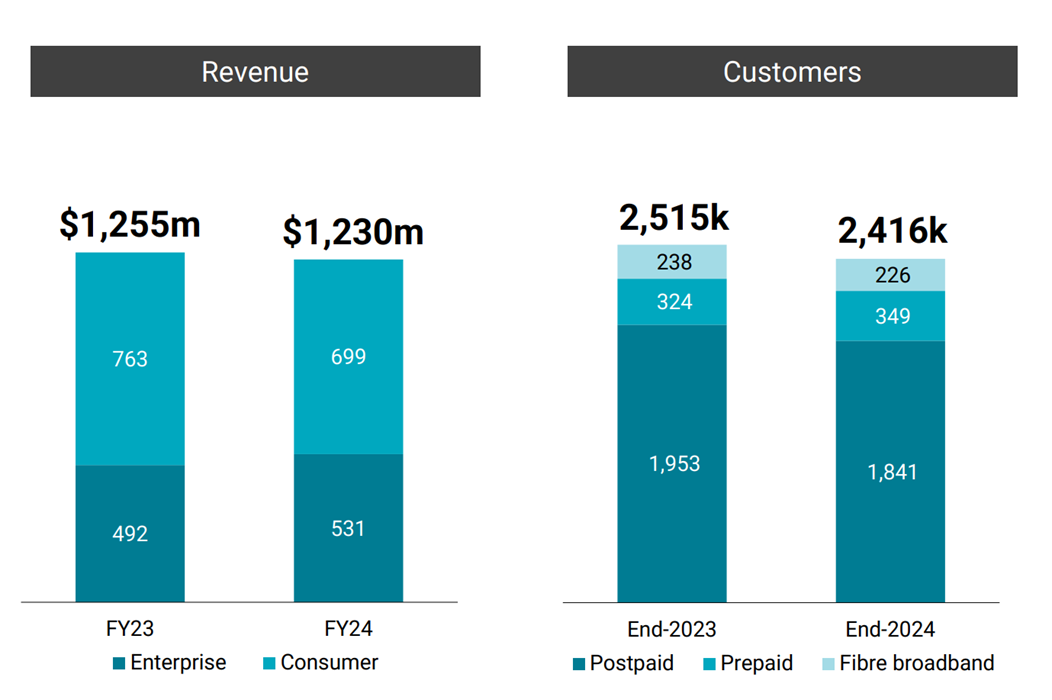

This was interesting for me but it turns out connectivity is basically just a solutions provider to (a) Telcos and (b) Data Centres.

The Telco business is basically M1 (acquired by Keppel), and nothing sexy to see here.

Revenue and customers are both down slightly, this is really just a mature business at this stage.

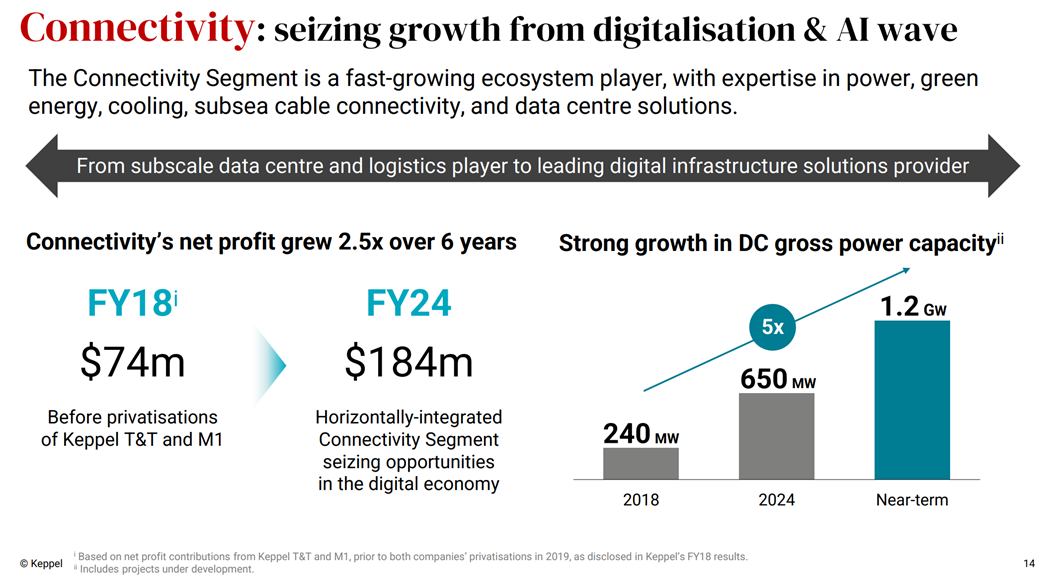

But data centres – boy that’s where things get really interesting.

Because we all know how hot AI is at the moment, and how much talk there is about AI requiring a massive buildup in global data centre infrastructure.

And if you really think about it, Keppel with its expertise in electricity / power, and data centres, could be pretty well positioned to benefit.

But here we need to separate the hype from the reality.

For now at least, data centre remains a small part of Keppel’s business – the bulk is still infrastructure and real estate as you see above.

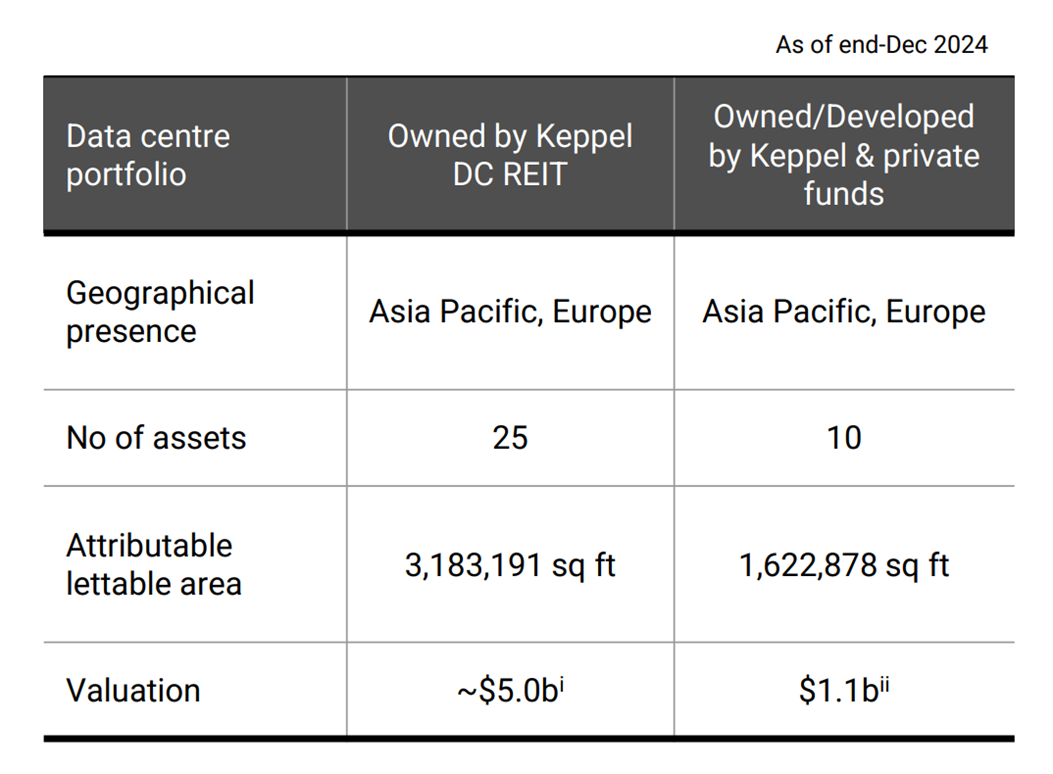

And yes, Keppel has 35 data centres under its infrastructure.

But to really grow from here – they need to win new contracts, new data centre buildouts.

And with Singapore tightly controlling the supply of new data centres in Singapore (due to constraints on the power grid), can Keppel deliver on this?

Will they be able to go into the APAC region, and win contracts for new data centre buildouts?

Frankly this is the exact same question I had for Singtel’s data centre business.

So far initial signs are promising, and you would think both Keppel and Singtel have what it takes to succeed in this business (Expertise + Temasek / Singapore name brand.

But hey – sometimes investors need to see the results before the share price can rerate.

And for now at least, Keppel remains primarily an old school, infrastructure / real estate / telco player.

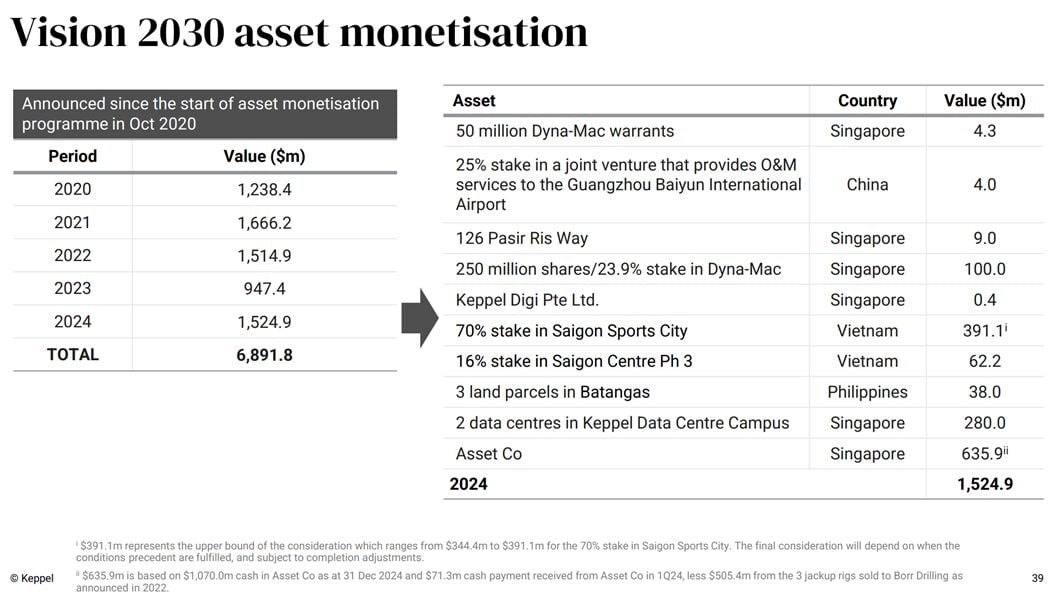

Similar to Singtel, Keppel also has an aggressive divestment / capital recycling plan.

They have “monetised” $6.8 billion in assets since 2020.

“Monetised” being a fancy word for sell, for those newer to corporate speak.

With $1.5 billion of that coming in 2024 alone.

Looking at the breakdown below, it generally looks like they are divesting their non-core assets and/or shifting assets off balance sheet into the REITs or fund vehicles.

This is fair, and to be expected in line with the strategy.

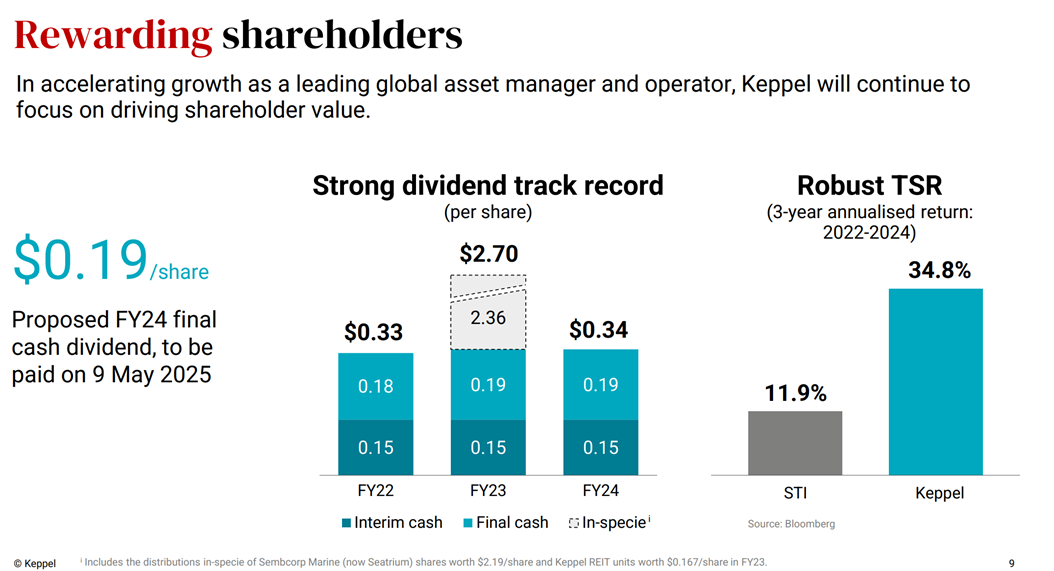

Keppel pays a $0.34 trailing dividend.

Which at latest share price of $6.84, works out to about a 5.0% dividend yield.

That’s pretty much in line with the dividend yields of Singtel, DBS, UOB and OCBC.

Annualised 3 year total shareholder return is a mind blowing 34.8% a year.

But if you look at the chart you’ll realise the bulk of that return came in the 2022 period post-Ukraine war.

And share price has been pretty much rangebound since 2023.

So the better question is where will Keppel’s share price go in the next year or two.

Follow Financial Horse to avoid missing any post!

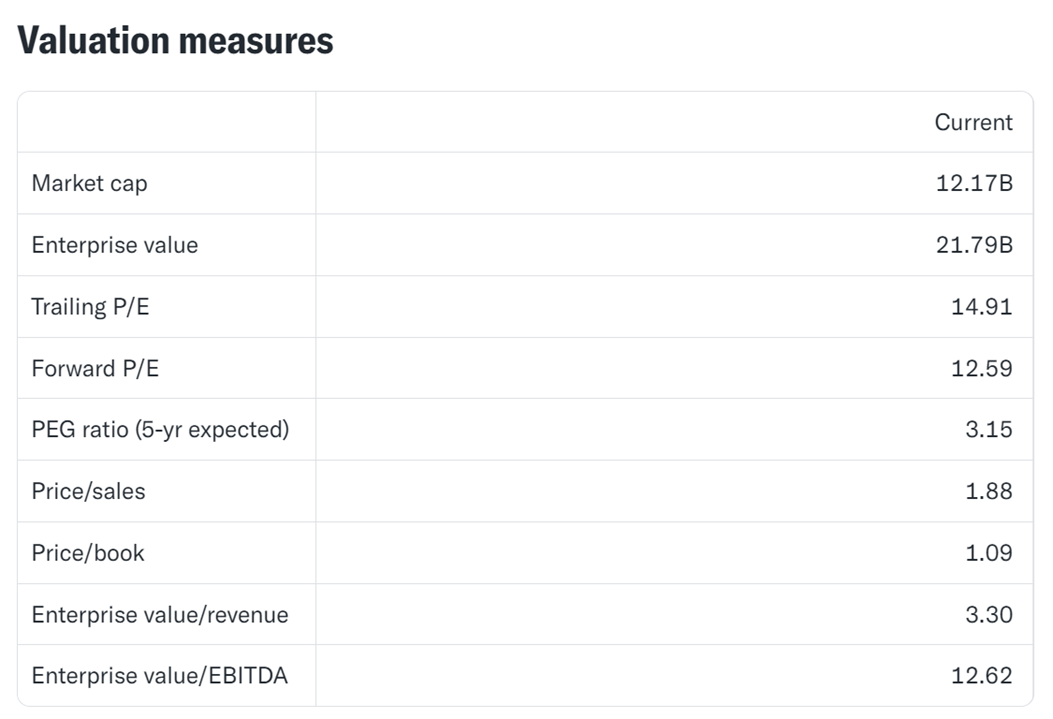

Trailing P/E is 14.9x which looks very cheap at first glance.

But when you really think about it – the bulk of the profits are coming from old school stuff like infrastructure (electricity generation) and real estate.

And the only sector growing profits meaningfully is the data centre business, which remains very small relative to the size of the overall business.

So yes I know PE looks “Cheap”, but I would venture some caution on placing too much reliance on this as Keppel is for now still a pretty old school kind of business without a lot of growth baked in.

Here’s the daily chart for Keppel.

It’s nothing much to shout about.

Yes I know it looks like it’s been trending up since Aug 2024.

But frankly look at the bigger picture and it’s fairly clear the stock is still rangebound for now.

Look at the moving averages on the daily chart – and it’s clear there’s no clear trend for now.

To sum up my views.

The infrastructure business is printing money at this stage – which gives Keppel a very solid base of profits to build on.

This is the main reason why the stock price has rallied so much since 2022 (okay that and the divestment of the loss-making marine business).

However, given that inflationary pressures are under control for now, I wouldn’t expect a huge jump in profits for infrastructure in the near term (although that said the upside potential if inflation returns is nice to have).

Meanwhile the real estate business.

There’s just so much you can do with real estate in this market, given that the structural tailwinds of zero interest rates or strong economic growth are no longer in place.

It goes back to that Buffett quote about “When a management with a reputation for brilliance tackles a business with a reputation for poor fundamental economics, it is the reputation of the business that remains intact.”

On Connectivity – Yes the data center part of the business is probably the sexiest and fastest growing part of Keppel today.

But unfortunately when compared to the overall size of Keppel, it’s still very small and unlikely to move the needle meaningfully by itself.

And there is significant uncertainty over execution.

I think bottom line for me.

I think Keppel is probably a decent buy, and valuations are decent.

Fundamentals wise, I get it, and I like it.

It’s why the article is titled “Why I may buy Keppel”.

But you know what – I can also see exactly why the stock has been rangebound for 2 years.

And short term – I don’t really see any catalysts on the horizon that would change that.

Which means that as an investor, you can pick up Keppel today and get the 5% dividend yield.

And wait around for something to change that sparks a meaningful rerating in the share price.

Or you can wait until a meaningful catalyst, and add at that stage (but of course you would miss out on the initial rally).

Personally for me, as much as I like the business on a fundamental basis, I don’t see an urgent need to add to Keppel at this stage.

There’s just too many opportunities in this market today, for me to put a big chunk of change into what could potentially be a lazy position that just trades rangebound for a while (you can see the FH Stock watch for list of stocks I am keen to buy).

Some of you may ask between Keppel and Singtel, which would I prefer.

As you would recall, a few weeks back I looked at Singtel and shared that I might actually buy a position in Singtel.

I would say fundamentals wise, I like both Singtel and Keppel equally.

But for some reason – the charts for Singtel look much better.

I wrote my article when the share price was at 3.10 and said that if it started to break out I could really see a big move coming.

Since then the share price has rallied all the way up to 3.42, back to 2024 highs.

If it continues going and breaks even higher – that could be really interesting for investors.

Whatever the case, you can see my full portfolio (with weekly updates), on FH Premium, where I share my most updated thoughts, and the stocks / REITs I am keen to add to.

This post is written on 14 Feb 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

A few weeks back, I looked at Singtel stock and concluded that I actually really liked what I saw. The transformation of Singtel looked promising, and the charts looked phenomenal. Along that line of reasoning. There’s another TLC that I’ve been monitoring for a while, and that I wanted to do a deep dive into. Keppel. What

The post Why I may buy Keppel stock at 5.0% dividend yield? Infrastructure play well positioned for the next decade? appeared first on Financial Horse.