Treasury bills (or T-bills in short) saw demand from retail investors spike in 2022 as interest rates rose from around half a percentage point to above 4%. Despite the investment element of the debt instrument, T-bills are considered to be as good as risk-free because they are issued and fully backed by the Singapore Government.

Due to the current high interest rate environment, the T-bills – which can be bought using cash, supplementary retirement scheme (SRS) funds, or CPF Investment Scheme (CPFIS) funds – provide an arbitrage opportunity for investors to safely beat the 2.5% returns on their CPF Ordinary Account (CPF OA).

Until recently, CPF members who wished to apply for the T-bills using the CPF OA funds had to open a CPF Investment Account with one of the three local banks (DBS, UOB, or OCBC) and apply in person at the bank branches.

However, CPF members who have a CPFIA with DBS can now skip the long queues and apply for the T-bills online through the DBS i-banking portal. Here’s how you can do so:

Read Also: Treasury Bills (T-bills): What Are They And How You Can Buy Them

Step 1: Log In To DBS iBanking

Log in to the DBS i-banking portal and select Singapore Government Securities (SGS) under the Invest tab. Select the Treasury bills (T-bill) option under the “Apply for Singapore Government Securities (SGS)” page.

Step 2: Apply For The T-Bill

If there is a T-bill available, you will be directed to the information page on the T-bill, as shown below. Click the apply button to proceed.

Step 3: Enter Your Personal And Investment Details

At this stage, you will see the details of the T-bill that you are applying and your personal details.

Here you must select the bid type – non-competitive or competitive bid – that you wish to make. Simply put, for a non-competitive bid, the yield does not need to be specified, and the applicant is allotted based on the uniform yield determined by the auction.

On the other hand, for a competitive bid, you would need to specify the yield (up to two decimal places). A lower yield would represent a more competitive bid, but it could also mean a possibly lower return than the uniform yield. If the submitted yield is higher than the uniform yield, there will be no allocation of the T-bill.

*Personal information (i.e., Name and NRIC) has been omitted from screenshots.

Once the bid type is selected, you would need to indicate your investment amount, which has to be in multiples of $1,000.

You also need to indicate choice of payment method (ie, cash, SRS, CPF-OA). Assuming you want to invest with your CPF-OA funds, select the relevant option.

Step 4: Confirm Your Application Details

Review your application details in this overview section. Ensure the payment method, T-bill issuance code, bid type (competitive/non-competitive), and investment amount are correct before submitting your application.

Once done, you will get a confirmation of your application. Thereafter, the appropriate CPF OA funds (less the discount based on the cut-off price) will only be debited after the successful allocation of the T-bills, closer to the issue date.

Read Also: How Much More Interest Will You Get If You Invest Your CPF Special Account In T-Bills Now?

What Else To Take Note When Applying For T-bill Using CPF OA Funds

Application Date

Online applications for investing in T-bills using cash or CPF OA funds start at 6 p.m. on the issuance’s date of announcement.

Applications ends one business day before the auction date at 9 p.m. for cash applications and ends two business days before the auction date at 12 p.m. when applying using CPF OA funds.

Transaction Costs

The transaction charge for online cash applications is waived on DBS i-banking, while a fee of $2.50 + GST (which, works out to $2.70) is required for CPF OA funds.

There is also a service fee of $2 (+ GST) charged per counter per quarter when using CPF OA funds. For example, if the T-bill issuance has a 6-month maturity period from January to June, the CPF member would incur a total of $4.32 for two quarters.

Opportunity Costs

CPF members using CPF OA funds to invest in T-bills would need to factor in the opportunity costs of investing the funds.

While T-bills generate simple interest, the interest earned on CPF OA savings is computed monthly and compounded annually. For instance, any contributions received this month would only start earning interest next month. On the other hand, any withdrawals made this month will not earn interest from this month forward.

For example, assuming a 6-month T-bill with the issuance date of 2 May and the maturity date of 31 October, you would lose 7 months of CPF interest if the funds were withdrawn in May and returned by November.

On the other hand, assuming a 6-month T-bill with the issuance date of 29 November and the maturity date of 30 May, it would result in losing 8 months of CPF interest if the funds were withdrawn by November and returned to CPF OA in June.

Issuance Date

Maturity Date

Loss Of Interest (Months)

02 May

31 October

7

29 Nov

30 May

8

Therefore, when investing using CPF OA, the issuance date and the maturity date are important factors to consider as it may mean losing less CPF interest for 8 months instead of the standard 7 months.

Read Also: Why Every Singaporean Should Apply To Invest Their OA Funds In T-Bill

Returning CPFIS Funds Back To CPF OA

If you no longer intend to invest after the T-bill matures, you should transfer the funds back to your CPF OA to avoid losing the CPF interest.

There are no charges for this request, and there is no minimum or maximum limit to the transfer amount. However, do note that it would take 3 business days for the fund to be transferred to the CPF OA.

To make the transfer, select the “More Investment Services” option under the Invest tab on the DBS i-banking portal. Thereafter, choose the “Refund to CPF Board” option under the Manage Investments column.

Here, you can indicate whether you would like to make a full or partial transfer of your funds in the CPFIS to your CPF OA.

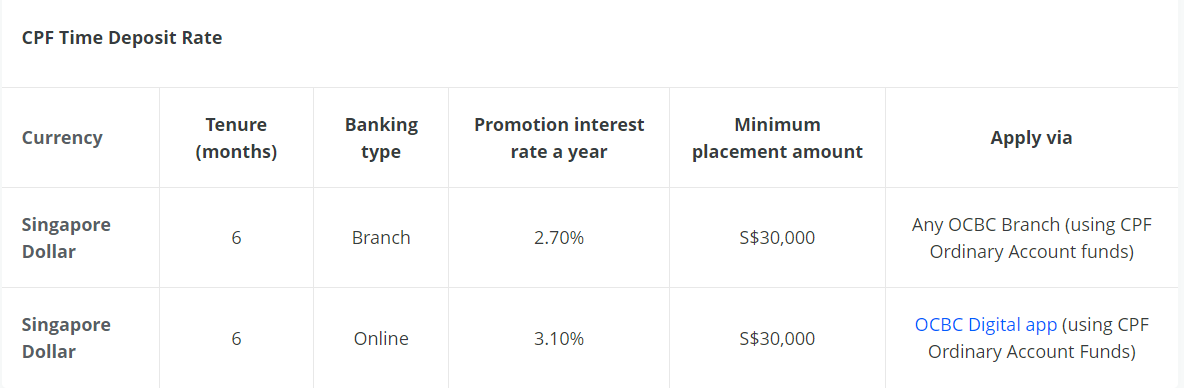

No Guesswork On The Yield And Investment Amount With OCBC’s CPF Fixed Deposit

Alternatively, CPF members can also choose to invest their CPF OA funds in a CPF Time Deposit offered by OCBC Bank.

Source: OCBC Bank

The advantage of the CPF Time Deposit is that it guarantees both the yield and investment amount, which are uncertain at the point of T-bill application. CPF members can earn 2.80% p.a. on either a 6-month or 12-month tenure when they apply using the OCBC Digital app.

Similar to the T-bills, you can only invest balances above $20,000 of your CPF OA funds, and it takes up to 3 working days to process the CPF Fixed Deposit application. If you wish to invest in the OCBC CPF Time Deposit, you must invest a minimum sum of $30,000 for each placement, while the upper limit is $999,999.

OCBC’s fixed deposit offer could be beneficial for investors who intend to invest more than $30,000 of their CPF OA and wish to reduce the uncertainty of the interest rate and allocation amount. However, investors may still want to calculate the opportunity and transaction costs to understand the potential gains before making any investment decisions.

Read Also: OCBC Is Now Offering 3.4% P.A. For CPFOA Fixed Deposit, But What’s The Catch?

This article was first published on 22 February 2023 and has been updated with the latest information.

The post Step By Step Guide To Buying T-Bills Online Using Your CPF OA Savings appeared first on DollarsAndSense.sg.