So I was reading this article titled “Will I Sell My OCBC Shares At All-Time Highs After its Dividend Cut” The article basically walks through OCBC’s latest earnings and dividend cut. Suggests that OCBC is expensively valued here. And then here’s the kicker. Concludes that OCBC is expensive enough that the author wouldn’t buy more […]

The post Will I sell my OCBC bank shares or buy more after the dividend cut? Buy DBS or UOB bank instead? appeared first on Financial Horse.

So I was reading this article titled “Will I Sell My OCBC Shares At All-Time Highs After its Dividend Cut”

The article basically walks through OCBC’s latest earnings and dividend cut.

Suggests that OCBC is expensively valued here.

And then here’s the kicker.

Concludes that OCBC is expensive enough that the author wouldn’t buy more shares at this price, but also wouldn’t be selling because his buy is price is below $10.

Personally I never understood the fixation about the price you bought a stock.

The way I see it, every day I own a stock, I have the option to sell at market price.

And choosing not to sell, means I am “buying” at the market price.

So I didn’t really agree with the thought process.

But the article was interesting enough that I wanted to walk through it and share some of my views.

Enjoy this exclusive FH Premium analysis—now free for all readers! But why stop here?

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea

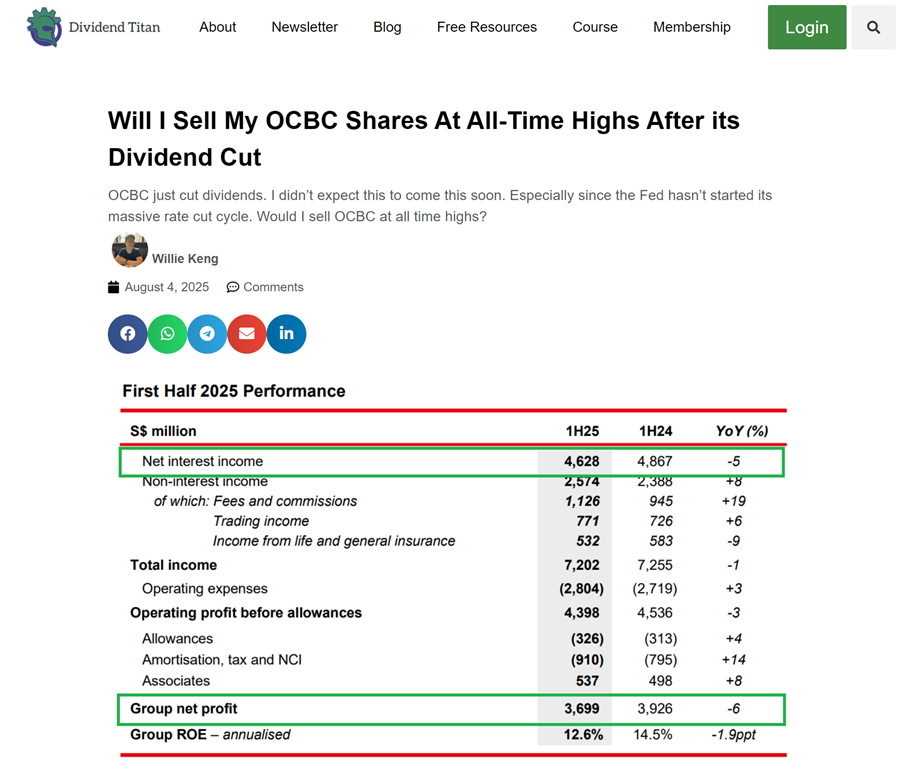

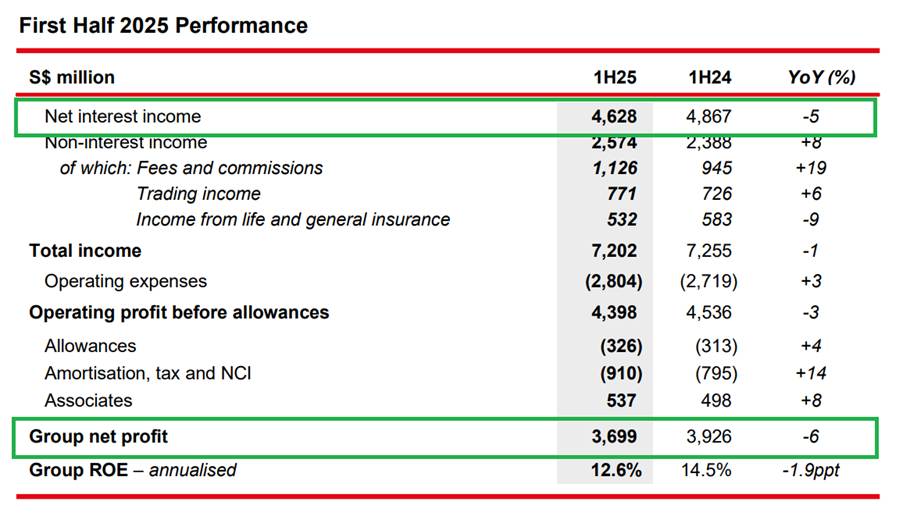

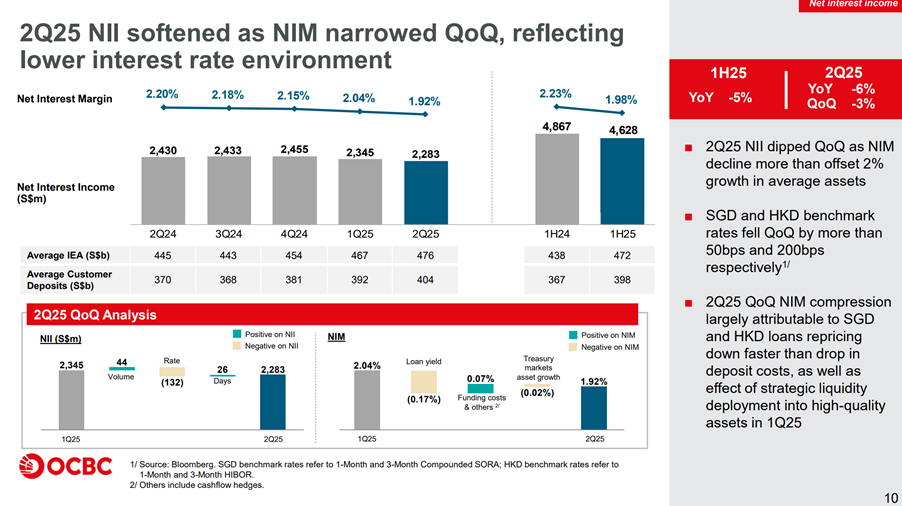

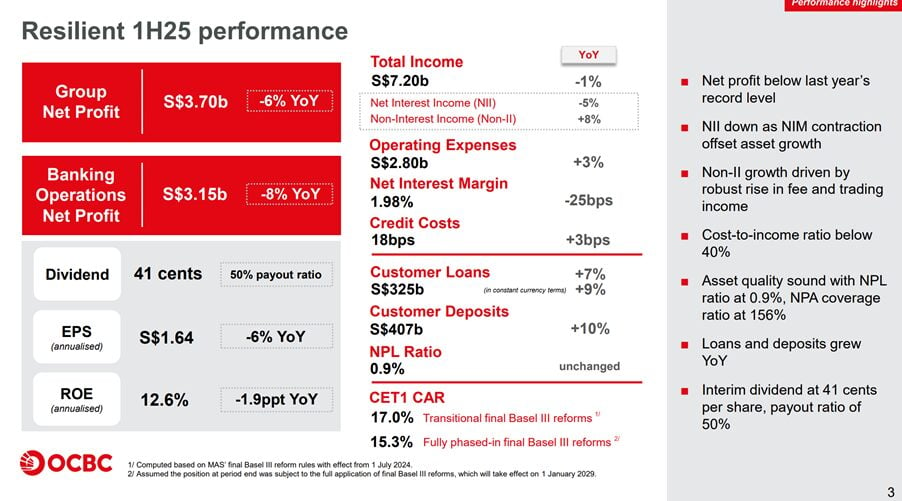

The full article is here, but let me summarise the key points below, and supplement with some charts from the latest quarterly presentation.

For ease of reading, I will summarise in bullet points.

- Margin squeeze for OCBC (and Singapore banks) has started due to lower interest rate environment

- Net Interest Income (NII) fell as benchmark rates dropped;

- Net interest Margin (NIM) compressed 12 bp to 1.92 %.

- Profit decline (down 6% year on year) signals peak-earnings phase for SG banks.

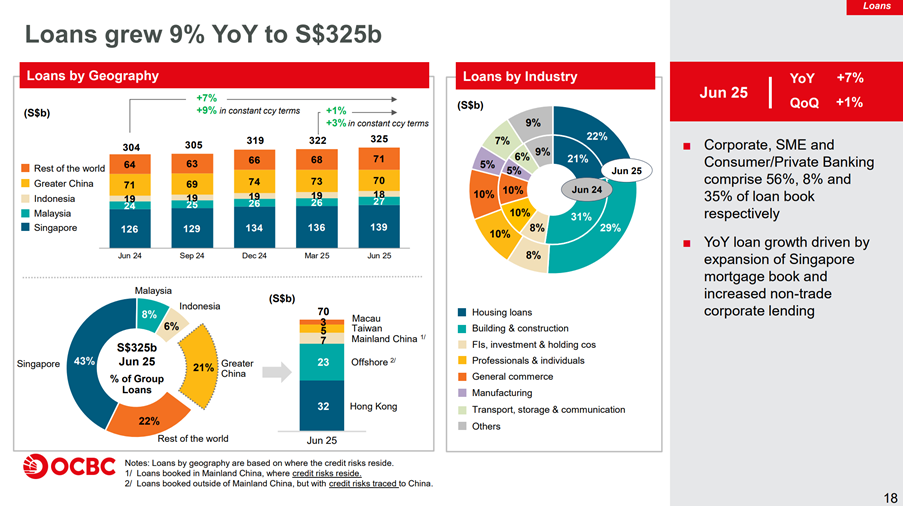

- Loan growth too weak to plug the gap

- Falling loan yields weren’t matched by higher volumes (or at least not big enough to offset lower interest rates), raising concerns about future profit and dividend momentum.

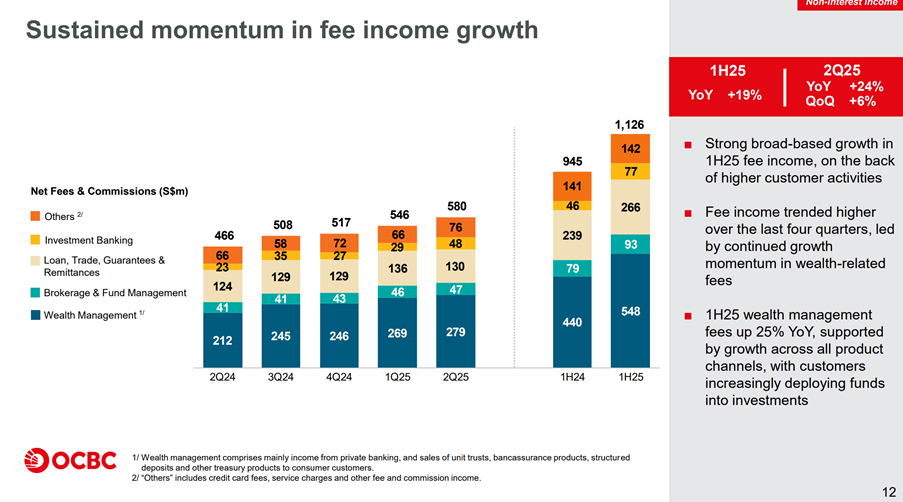

- Wealth-management is the bright spot

- Fee income +19 % YoY;

- Wealth income hit S$2.66 bn and AUM a record S$310 bn,

- Now 37 % of total revenue.

Here’s the big one, so let’s spend a bit more time talking about it.

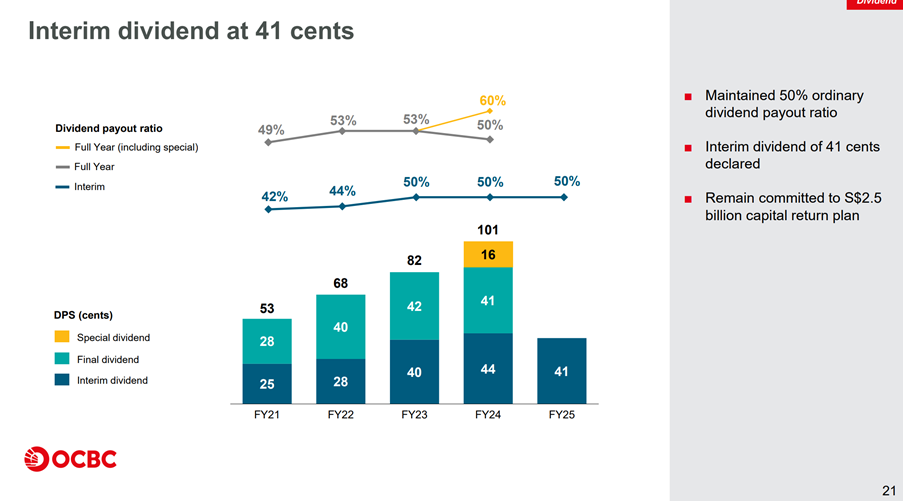

The interim dividend for OCBC has been cut from 44 cents last year, to 41 cents this year.

This is because OCBC wants to maintain a 50% ordinary dividend payout ratio.

So if the profits go down, it makes sense that the dividend will go down.

But you can see from the chart below that OCBC declared a special dividend in 2024.

This special dividend brought the final payout ratio up to 60%, and would artificially “juice” the dividend yield (assuming it is continued this year).

Long story short – because profits are down, the dividend for OCBC is down.

But for now at least, I would hardly say it is a catastrophic drop.

You can see how the share price dipped slightly after the recent earnings, but you could also chalk that up to general market volatility as the market prices in more rate cuts.

So the conclusion from the author on whether he would sell?

- Valuation risk is elevated

- At ~1.4× P/B, OCBC trades above historical norms, leaving “not enough margin of safety” for new buyers.

- Reminder: the last time the stock hit 2× P/B (2007) it later fell >55 %.

- Hold, don’t fold—if your cost is low

- Author bought < S$10; comfortable yield-on-cost justifies holding but not averaging up.

- Dividend yield vs DBS and UOB Bank is marginal —hardly enough to outweigh valuation risk.

- OCBC Bank: 5.06% dividend yield

- DBS Bank: 4.99% dividend yield

- UOB Bank: 4.89% dividend yield

Basically, his view is that because he about below S$10, his yield on cost is great and justifies holding the position.

But because OCBC at 1.4x Price to Book looks pricey, he doesn’t want to add more.

Okay now I have quite a bit of thoughts on the analysis above, but let me break it down into 3 points.

- Investing is about how much you make when you’re right, vs how much you lose when you’re wrong

- The price I buy a stock at, means absolutely nothing to me – only the price the stock trades at today.

- Will I sell my OCBC shares or buy more?

If there’s one thing that I’ve learned in investing.

Is that frankly, it matters very little to me whether I am right or wrong.

I have my view on a stock, but if the facts change, I can easily change my view overnight.

I don’t bring any ego into my investing, and when I am wrong on something, I have no problem admitting so.

What matters more to me – is how much I make when I am right, vs how much I lose when I’m wrong.

What do I mean when I say this?

Is that I want to buy stocks where if I am right, I can put $100 in and make $500.

And if I am wrong, I only lose $50.

And not investments where if I am right I make $50, and if I am wrong I lose $50.

Let’s try to apply that thought process to OCBC bank.

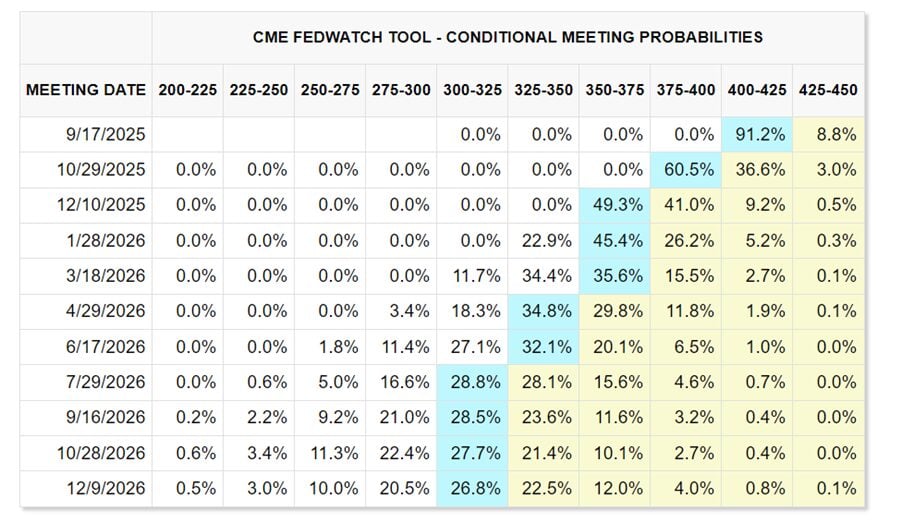

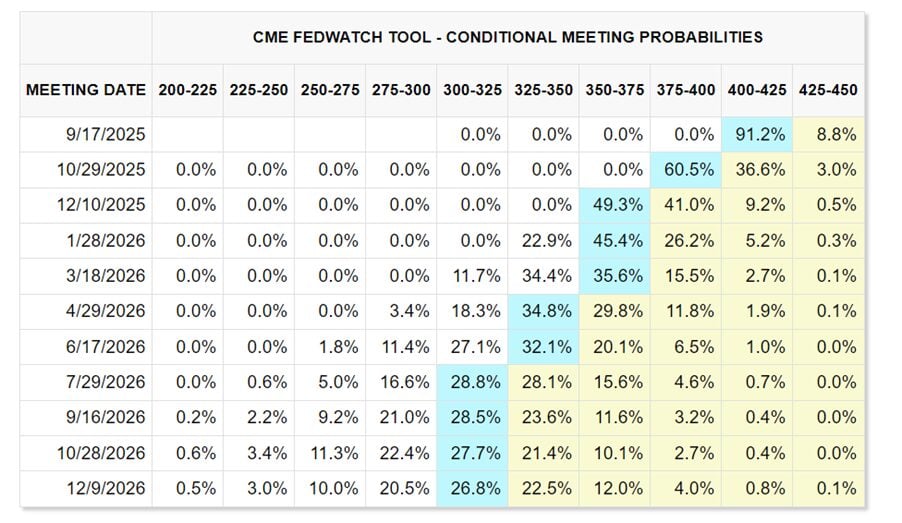

We know that we’re in a declining interest rate environment today.

I mean Jerome Powell’s term is going to be up soon, and you pretty much know that Trump is going to appoint someone who is going to cut interest rates.

This is why the market has priced in so many rate cuts over the next 12 months:

We’ve seen above that a lower interest rate climate does hit bank profitability, so this does place some cap on the upside potential for the banks.

Crunching some high level numbers.

OCBC Bank’s book value is 12.92, and it trades at a 1.32x book value today.

Let’s say things go smoothly, and OCBC goes back to the early 2025 highs of 1.4x book value.

That’s about a 6% capital gain upside.

Throw in the 5% dividend yield, and you’re looking at a 11% upside in the next 12 months.

So that’s how much you make if you’re right.

Okay if we get a global recession and rate cuts are slashed, then it could go all the way back to book value or lower.

But I think that’s an extreme tail risk situation, so it wouldn’t be my base case.

Let’s say economic growth slows, and interest rates are cut by the new fed chair.

And investors turn bearish on bank stocks.

Let’s say OCBC bank goes back to 1.12x book value, which was the low hit during the April “Liberation Day” tariffs selloff.

That’s about a 15% capital loss.

Add back the 5% dividend.

And you’re looking at a 10% loss.

Putting that together.

If I’m right and things go well.

That’s a 10% gain for me.

If I’m wrong and things head south.

That’s a 10% loss for me.

And sure you can argue that the probability that I am right and the 10% gain materializes is higher than the downside case.

But how much higher is it?

Would you be willing to say that the upside case is 80% probability, and the downside 20%?

I frankly don’t know.

Which puts me in a situation where if I am right I don’t really make a lot of money, vs how much I lose when I am wrong.

Which brings me to my second point.

You would note that nowhere in my analysis did I consider at what price I bought OCBC bank originally.

In fact if you ask me now what is my average buy in price for OCBC bank – I frankly have no clue.

That is how little importance I place on my buy in price.

The way I see it.

After I buy a stock, I immediately forget the price I bought it.

The beauty of investing in public markets, is that every day I can look at the quoted price and decide if (a) I want to buy more, or (b) I want to sell my position.

And every day that I choose to do nothing, I am effectively saying that I am happy owning OCBC bank at today’s market price (because otherwise I would just have sold at market price).

That’s why I never bother with the price I bought a stock.

And that’s why I found it unusual the author of the article above places so much importance on the fact that he bought below $10.

I mean I can understand the thought process – but to me it is an irrelevant consideration.

If you think OCBC is expensive at $14, you should be locking in the profits and rotating into other stocks with higher upside potential.

Never miss a market beat—ride with Financial Horse wherever you go!

Get timely insights, sharp analyses, and real-time alerts by subscribing or following us on your favorite platform:

Subscribe to our mailing list for exclusive content straight to your inbox, plus early access to special reports and FH Premium previews

Which brings us to the final question.

After running through the analysis above – would I sell my OCBC shares after the dividend cut, or would I buy more?

As I like to do recently, I asked the new ChatGPT 5 Thinking model.

The answer:

- Call: HOLD. Add on dips; not a sell unless it re-rates.

- Buy zone: ≤ 1.25× P/B (≈≤ S$16.1) or ≥5% fwd yield (≈≤ S$16 on ~S$0.82 DPS).

- Trim/Sell: ≥ 1.45× P/B (≈≥ S$18.7) or if NIM <1.90% / payout weakens.

- Setup: Rate cuts compress NIM; NII guidance cut; near-term earnings flat-to-down.

- Offsets: Strong capital (CET1 ~17%), low NPLs, wealth-fee growth; ~60% total payout and buybacks support yield.

- Optionality: Great Eastern integration upside delayed after failed delisting.

- Watch: 3Q25 NIM trend (≥1.90%?), fee momentum, CET1 ≥16.5%, credit costs.

- Action: Keep for income and optionality; accumulate sub-S$16; reassess after 3Q25.

I don’t know who it was, but a reader left a comment that ChatGPT makes for a scarily good investment analyst.

And I absolutely agree.

Because ChatGPT’s answer above is very, very close to my own personal views.

I find these days that LLMs will get you 80-90% of where you need to go.

Then you add that final human touch yourself.

I find it hard to get excited about banks here.

I don’t find them particularly cheap.

And risk for interest rates is tilted towards the downside in the short term.

Just look at the amount of rate cuts priced in.

And the stunning drop in Singapore 10 year yields:

Because of that, my gut feel is that near term upside potential is capped.

But at the same time, I also don’t see a need to sell OCBC bank just yet.

The stock is still holding above the 50, 150 and 200 day moving averages.

Yes earnings are dipping, but it is hardly catastrophic.

And beyond the core lending business, wealth management is growing well, and the 5% dividend is still decent.

And longer term, I actually think the Singapore banks are a fantastic business model, a proxy play on the strength of the Singapore economy.

I have a position in OCBC bank, and I don’t see a need to sell unless the technical or fundamental picture deteriorates further (and if it does, like I said I can change my mind overnight – latest views are shared on FH Premium).

And if we get a decent dip, who knows I may just add to my position.

The final point I would add.

Is that position sizing matters too.

Is OCBC bank 5% of your portfolio today.

Or is it 30% of your portfolio today?

At this point in the interest rate cycle, my exposure to REITs is higher than it is to the Singapore banks.

So that’s why it may make sense for me to continue to hold.

But if your portfolio is 90% Singapore banks and 10% REITs, then you know what the answer may be different for you.

Whatever the case, you can see my full portfolio breakdown shares on FH Premium to understand how I am positioned.

Unlock Your Financial Edge with FH Premium

Enjoy this exclusive FH Premium analysis—now free for all readers! But why stop here?

By subscribing to FH Premium, you’ll gain:

- Weekly Macro Deep-Dives

Understand where the global economy is headed—and why it matters for your wallet. - Regular Buy/Sell updates from my personal portfolio

See exactly what I’m adding to (or trimming from) my portfolio and act before the crowd. - Comprehensive Watchlists

Full stock & REIT watchlists, updated regularly with target prices, entry zones, and risk considerations. - My Personal Portfolio

Transparent tracking of every position I hold—and why—so you learn the “what, why, and how” of smart investing.

Join hundreds of savvy readers who’ve turned FH Premium insights into real returns. Ready to level up your investing?

Subscribe to FH Premium today and never miss a market-moving idea

So I was reading this article titled “Will I Sell My OCBC Shares At All-Time Highs After its Dividend Cut” The article basically walks through OCBC’s latest earnings and dividend cut. Suggests that OCBC is expensively valued here. And then here’s the kicker. Concludes that OCBC is expensive enough that the author wouldn’t buy more

The post Will I sell my OCBC bank shares or buy more after the dividend cut? Buy DBS or UOB bank instead? appeared first on Financial Horse.