So it has been a long time since my last article on DBS Bank. And I know that DBS Bank is probably the most popular and most followed stock among Singapore investors today. So… let’s have a look at DBS Bank today. At $44.53, paying a 6.7% forward dividend yield. Will I buy DBS Bank […]

The post Will I buy DBS Bank stock at a 6.7% dividend yield? Compared vs OCBC and UOB Bank? appeared first on Financial Horse.

So it has been a long time since my last article on DBS Bank.

And I know that DBS Bank is probably the most popular and most followed stock among Singapore investors today.

So… let’s have a look at DBS Bank today.

At $44.53, paying a 6.7% forward dividend yield.

Will I buy DBS Bank stock today?

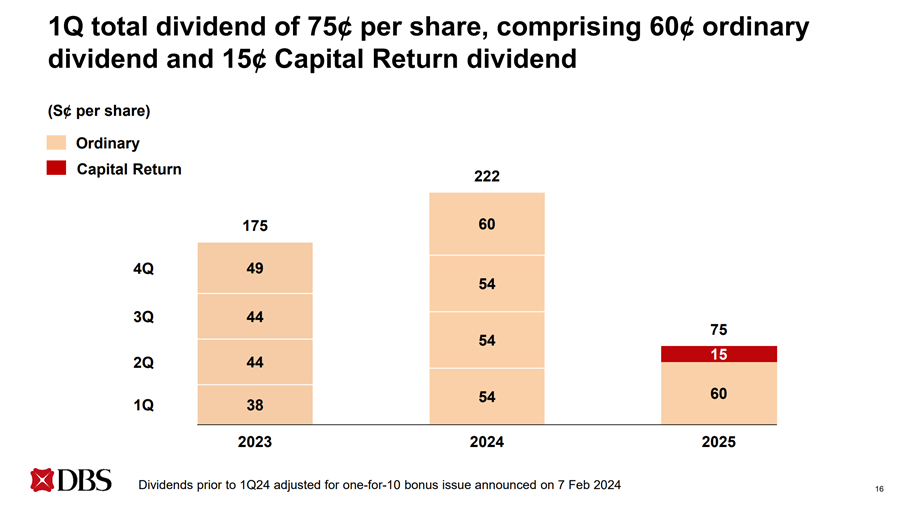

DBS Bank declared a 75 cents dividend for the most recent financial quarter.

Of which 60 cents is ordinary dividend, and 15 cents is capital return.

If you assume the 75 cents dividend will continue to be paid going forward.

Then annualising the 75 cents dividend, at $44.53 share price.

Works out to a 6.73% dividend yield for DBS Bank stock.

Very, very decent.

This is an FH Premium post.

I am making this available to all readers to keep you updated on my latest thinking given the current market volatility.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

But of course.

You will argue that 15 cents of that dividend is “capital return”.

How sustainable is this dividend?

I got ChatGPT o3 to crunch the numbers on DBS Bank’s 1Q 2025 dividend-payout ratio”

| Metric | Source line(s) | Figure |

| Net profit (1Q 25) | Trading-update table | S$ 2.897 bn DBS Bank |

| Total dividends declared (60 ¢ ordinary + 15 ¢ capital-return) | Dividend section | S$ 2.130 bn DBS Bank |

| Per-share EPS (annualised) | Per-share data | S$ 4.11 ⇒ S$ 1.03 for the quarter (4.11 ÷ 4) DBS Bank |

Payout-ratio calculations

| Basis | Formula | Result |

| Including the 15 ¢ capital-return element (75 ¢ total) | 2.130 ÷ 2.897 | ≈ 73.5 % |

| Ordinary dividend only (60 ¢) | (2.130 × 0.8) ÷ 2.897 | ≈ 58.8 % |

Answer: Using the full S$0.75 per-share distribution, DBS’s latest dividend payout ratio is about 74 % of 1Q 2025 earnings.

On the traditional measure that considers only the ordinary 60-cent dividend, the ratio is roughly 59 %.

74% dividend payout ratio if you include the “capital return”.

Boy that’s really on the high side, and rapidly approaching REIT levels.

So yes the 6.7% dividend yield is juicy and all.

But my gut feel is that at these levels DBS would be hard pressed to raise the dividend yield significantly from here on out.

And if there is any earnings impact from a slower economy, the dividend could be at risk of being reduced back to the ordinary dividend of 60 cents only (the 59% payout ratio is much more sustainable).

That would work out to a 5.38% dividend yield, bringing DBS in line with UOB and OCBC Bank.

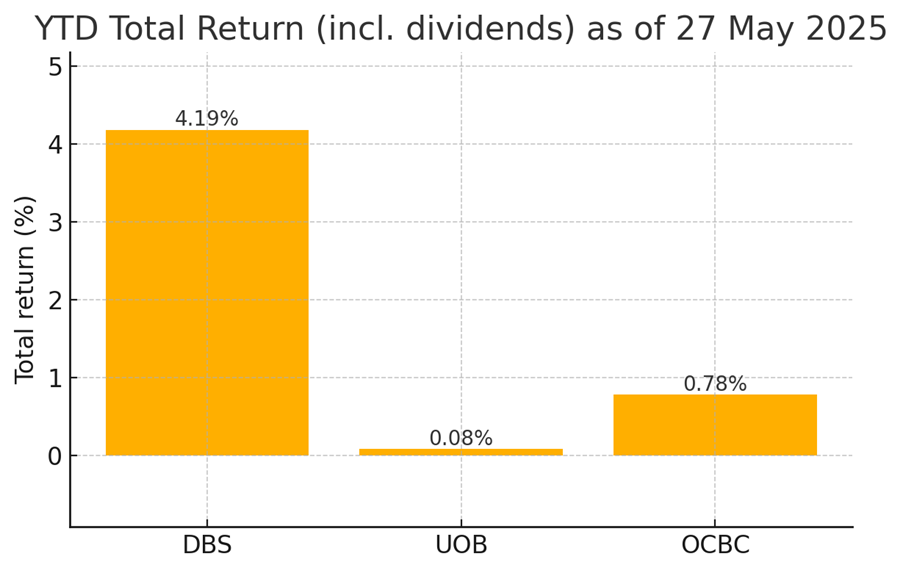

For what it’s worth though, DBS Bank has the highest return year to date among the 3 local bank stocks (after accounting for dividends).

You can also see the chart for DBS Bank below.

After the sharp drop below the 200-day moving average following the Trump Liberation Day tariffs, DBS’s stock price has largely recovered to where it started the year:

Let’s take a closer look at the financial results for DBS Bank.

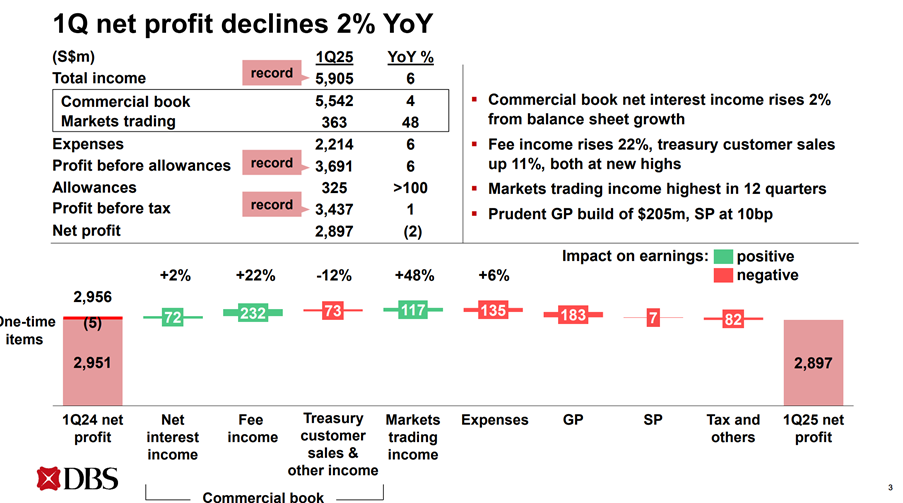

Q1 net profit is down 2% on a year-on-year basis.

But looking at the underlying numbers tells a very interesting story.

Because Net Interest Income is actually up 2%.

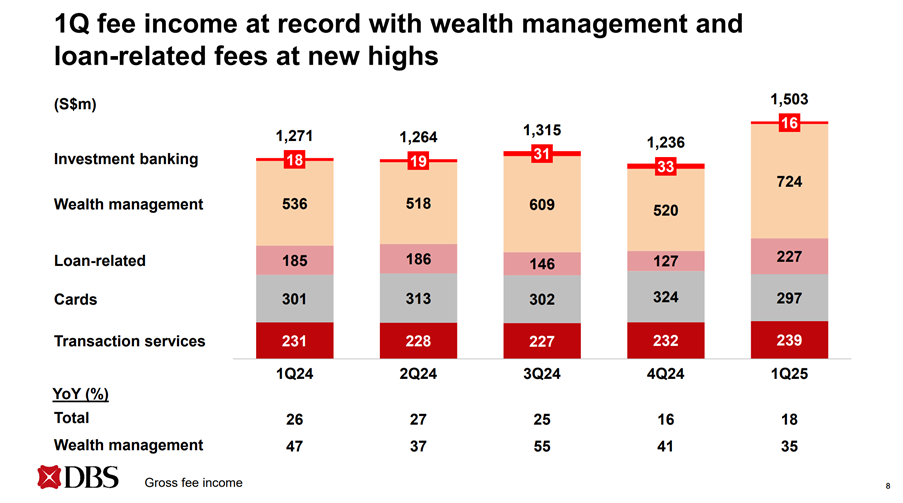

Fee income is up a whopping 22%.

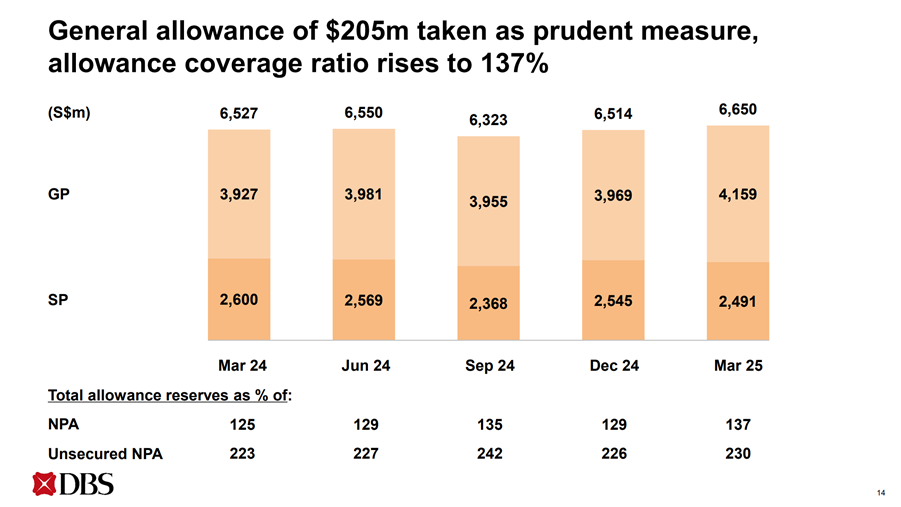

In fact the reason earnings is actually down (and not up) on a year on year basis is largely because of a $205 million general allowance that DBS Bank recorded.

So what exactly is this $205 million general allowance about?

Here are the exact remarks from senior management:

| Source | Exact remarks |

| CFO Chng Sok Hui – 1Q-25 results briefing (8 May 2025) | “*We added S$205 million of general allowances as a prudent measure given the recent escalation in macro-economic and geopolitical uncertainty. The increase *was not driven by any deterioration in our portfolio’s credit performance. Specific allowances remained low at 10 bp.” |

| CEO Tan Su Shan – same call | “Our GP reserves reflect prudence amid tariff uncertainty. Stress-test overlays now stand at S$2.6 billion (≈60 bp of loans); we deem that sufficient.” |

| DBS news release & Reuters report | “General allowances of S$205 million were taken to strengthen reserves to S$4.16 billion in light of heightened macro and geopolitical risks.” |

In plain English:

- Why add it?

Management sees rising external risks (fresh trade-tariff tensions, volatile rates, geo-politics) and decided to top-up provisions while profits are strong, so the loan book is protected if conditions sour. - Is credit quality worsening?

No. NPL ratio stayed at 1.1 % and specific allowances were only 10 bp—management stressed the charge is purely forward-looking.

- How big is the buffer now?

Total general-provision reserves rose to S$4.16 bn (≈1 % of loans), of which S$2.6 bn is an overlay for severe stress scenarios. - Bottom line

The S$205 m general allowance is a prudential overlay—essentially insurance against an uncertain macro backdrop, not a reaction to any immediate credit problems.

Personally if you ask me, this does look like a fairly conservative move by DBS Bank.

They probably just decided to top up provisions while profits are strong, to provide for the possibility for weaker economic growth arising from the Trump tariffs.

Again I think this is conservative from management, and I’m not sure current macro calls for such a large provision.

But hey what do I know, I’m just a financial horse…

As the famous Stanley Druckenmiller quote goes.

You don’t buy a stock for where it is today, you buy a stock based on where it is going to be in 18 months.

Let’s fast forward to end 2026.

What does the world look like then, halfway through the Trump administration?

Nobody knows what Trump is going to do, so trying to predict this with any degree of certainty is a fool’s errand.

So I figured let’s flip it around.

What will not change by end 2026?

And the key issue that popped up in my mind – inflation.

Or to be more specific, the US budget deficit, and where long term interest rates will trade.

All signs suggest that the US budget deficit is out of control, and it likely to remain that way even in late 2026.

Despite a strong start by Elon Musk’s DOGE to reduce government expenses, it seems like they have largely given up on those efforts, and current spending cuts are not enough to move the needle on the budget deficit.

Increased revenue from the tariffs will help no doubt.

But then on the spending side, Trump is likely to go ahead and pass tax cuts.

And gun to my head, from now until late 2026, I’m willing to bet he’s probably going to end up spending more than he saves.

The market seems to have sniffed this out too, because US 10 year yields are back up to 4.5% as we speak.

I suppose – not too poorly frankly.

If inflation stays elevated, long term interest rates stay high, and economic growth stays resilient.

I could see bank stocks performing decently well in that environment.

Sure you probably won’t see massive upside in share price.

But the profits will hold steady, which allows the dividends to be maintained.

Follow Financial Horse to avoid missing any post!

Let’s take a look at valuations of DBS Bank, compared to UOB and OCBC Bank:

| Price-to-Book (P/B) | Forward Dividend Yield | Return on Equity (ROE*) | |

| DBS Bank | 1.84 × | 6.8 % | 17.3 % |

| UOB Bank | 1.19 × | 5.2 % | 13.3 % |

| OCBC Bank | 1.18 × | 5.1 % | 13.7 % |

*ROE figures are the latest full-year FY-2024 numbers except DBS, whose Q1-2025 annualised ROE is shown (the FY-2024 record was 18.0 %).

DBS stands out from the pack here.

Yes, it is the most “expensive” at 1.84x book value.

But it also has the highest return on equity at 17.3%, and the highest forward dividend yield at 6.8%.

So you could argue that DBS Bank isn’t expensive, it’s fairly valued.

Coming back to the question.

Will I buy DBS Bank stock at 6.7% dividend yield?

In the spirit of full disclosure, I hold positions in the local banks, and you can see my full portfolio breakdown on FH Premium.

Will I add more exposure today?

Frankly – I don’t think so.

Like I said I have exposure, so if prices go up I do benefit.

But at these prices, I continue to struggle to find risk-reward incredibly compelling.

Even in the best case macro outcome, with strong economic growth and no inflation, you’re looking at maybe 10-20% share price upside.

In the worst case macro outcome, with a global economic slowdown, there could be a fair bit of downside.

Just to be clear, I am not saying that DBS Bank is a bad investment.

I am saying that at this price, I don’t find the risk-reward compelling, and I just don’t see myself adding to positions at these prices.

And to be absolutely honest after the recent stock rally over the past 1.5 months, I don’t find stock valuations particularly attractive given the global macro climate.

Sure there are pockets of value, and you can see my thoughts on where value lies in the FH Stock Watch on FH Premium.

But by and large, I don’t find stocks particularly cheap today.

Just to be clear again.

While I don’t find stock valuations particularly attractive.

I continue to hold significant stock exposure to US, China, Singapore, Bitcoin and Gold.

I just don’t think there’s any way around it, because in an inflationary / money printing climate you do need that kind of exposure that could hedge inflation.

What I’m doing to hedge risk, is to balance out that allocation with a healthy allocation to cash, bonds, fixed income, REITs etc.

In a climate when you can get 3-5% yield for generally low – moderate risk, I think there’s a good case for having decent allocation to cash / bond products today.

The exact split – that goes back to risk appetite.

But hey that’s just me, and you can see my full portfolio breakdown on FH Premium.

Love to hear what you think! Would you buy DBS Bank at 6.7% dividend yield?

This is an FH Premium post.

I am making this available to all readers to keep you updated on my latest thinking given the current market volatility.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

So it has been a long time since my last article on DBS Bank. And I know that DBS Bank is probably the most popular and most followed stock among Singapore investors today. So… let’s have a look at DBS Bank today. At $44.53, paying a 6.7% forward dividend yield. Will I buy DBS Bank

The post Will I buy DBS Bank stock at a 6.7% dividend yield? Compared vs OCBC and UOB Bank? appeared first on Financial Horse.