I’ve been getting a lot of questions about China of late. Because of the US-China tariffs, China stocks have sold off, which presents opportunity for investors who believe in either: Plus the sell-off has made valuations more attractive than where it was at the start of the year. UOB Asset management recently launched a new […]

The post How to invest in China as a Singapore Investor? Is it a good time to buy China stocks? appeared first on Financial Horse.

I’ve been getting a lot of questions about China of late.

Because of the US-China tariffs, China stocks have sold off, which presents opportunity for investors who believe in either:

- The long term growth potential of the China market, or

- The short – mid term potential for further stimulus from Beijing

Plus the sell-off has made valuations more attractive than where it was at the start of the year.

UOB Asset management recently launched a new ETF that tracks the FTSE China A50 Index, which provides a simple and fuss free way for Singapore based investors to invest in China A-shares via the SGX.

So I was quite keen to do a deeper dive to understand more.

Disclosure: This post is sponsored by UOB Asset Management. All views and opinions expressed in this post are from Financial Horse. This advertisement has not been reviewed by the Monetary Authority of Singapore. This does not constitute as financial advice and you should seek advice from a financial adviser, or consider whether the portfolio is suitable for you.

The ETF in question is UOBAM FTSE China A50 Index ETF.

It seeks to replicate as closely as possible, before expenses, the performance of the FTSE China A50 Index.

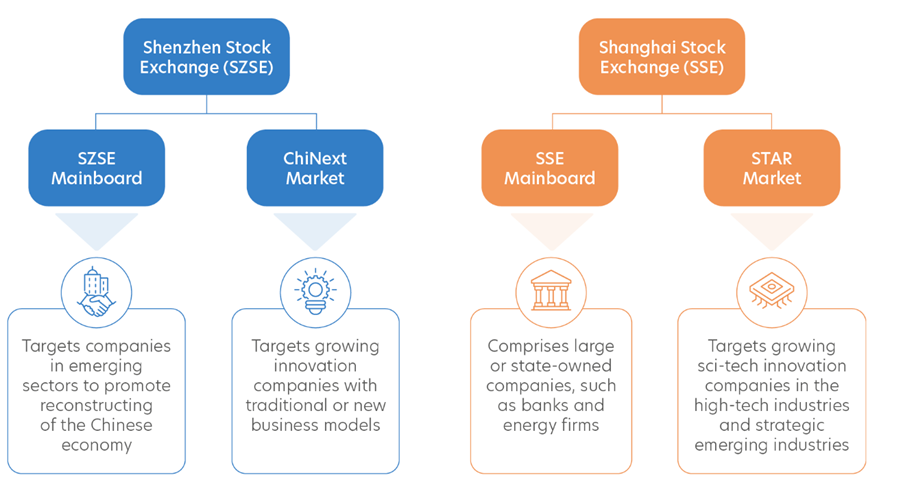

The FTSE China A50 Index is free-float market capitalisation-weighted and consists of the 50 largest A-share stocks listed on the Shanghai and Shenzhen stock exchanges.

You can see more on the benefits of tracking the 50 largest A-share stocks listed on the Shanghai and Shenzhen stock exchanges below:

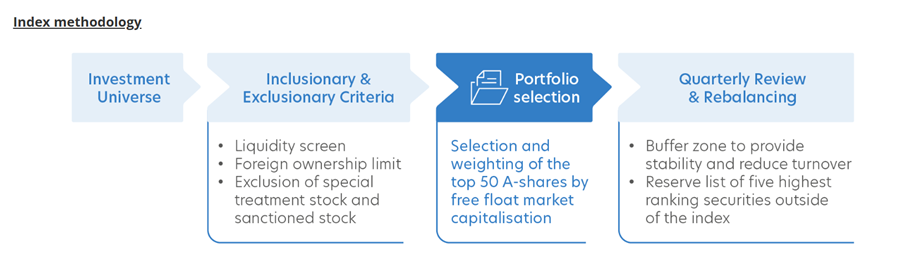

Simple and predictable composition

- Free float market capitalisation approach; constituents with higher capitalisation are assigned higher weightings

- No complex index methodology that might introduce higher unsystematic risks

Low index turnover

- Largest stocks typically retain their dominant positions, leading to lower index turnover during rebalancing

- Reduces transaction costs for passive management approach

Quarterly rebalancing

- Quarterly review and rebalancing in March, June, September and December which aligns with earnings season and China central bank meetings

- Buffer zone provides stability and reduces the turnover of the index

Represents the China A-Share market

- While the Index has a small number of constituents, it represents about a third of the broader China A-share market, based on market capitalisation1

- Highly correlated to the broader China A-share market based on historical performance2

1FTSE Russell, as of 31 December 2024

2Bloomberg, September 2024. Based on weekly total return performance data in CNY for the past 10 years.

What exactly will you be buying into?

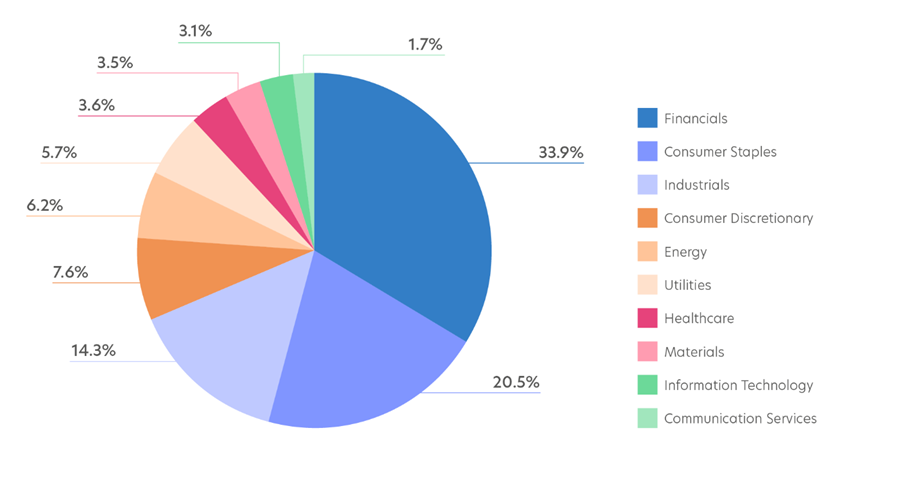

High level asset allocation is set out below, and the top 5 sectors are:

- Financials – 33.9%

- Consumer Staples – 20.5%

- Industrials – 14.3%

- Consumer Discretionary – 7.6%

- Energy – 6.2%

Source: UOB Asset Management, retrieved on 3 June 2025

Source: UOB Asset Management, retrieved on 3 June 2025

Top 10 holdings are:

| Company Name | % Holding |

| KWEICHOW MOUTAI CO LTD | 11.94 |

| CONTEMPORARY AMPEREX TECHNOLOG | 6.26 |

| CHINA MERCHANTS BANK CO LTD | 5.16 |

| CHINA YANGTZE POWER CO LTD | 4.43 |

| BYD CO LTD | 3.94 |

| PING AN INSURANCE GROUP CO OF | 3.36 |

| INDUSTRIAL & COMMERCIAL BANK O | 3.32 |

| WULIANGYE YIBIN CO LTD | 3.08 |

| AGRICULTURAL BANK OF CHINA LTD | 2.86 |

| INDUSTRIAL BANK CO LTD | 2.66 |

Source: UOB Asset Management, retrieved on 3 June 2025

Source: UOB Asset Management, retrieved on 3 June 2025

Some potential benefits of the UOBAM FTSE China A50 Index ETF are set out below.

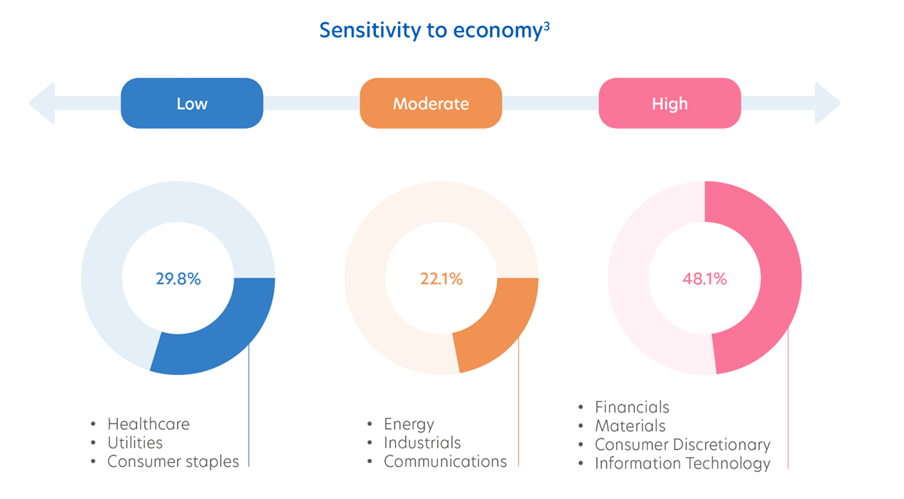

Sectors like Healthcare, Utilities and Consumer Staples are less sensitive to the economy, and continue to do well even in a weak economic climate.

At the same time, there is exposure to the sectors like Financials, Materials, Consumer Discretionary and Information Technology that would do well if the China economy were to pick up[1].

Source: FTSE, as of 31 January 2025

And because the UOBAM FTSE China A50 Index ETF is primarily made up of large cap stocks, this does provide stability in the form of higher upside during rallies, and (comparatively) lower drawdowns during market corrections – compared to other all-cap indices such as the FTSE China A All Cap Index.

Source: FTSE, as of 31 January 2025

The UOBAM FTSE China A50 Index ETF is also listed on the SGX.

And you can invest in the ETF using either cash or SRS Funds.

Both SGD and USD share classes are available depending on your preference.

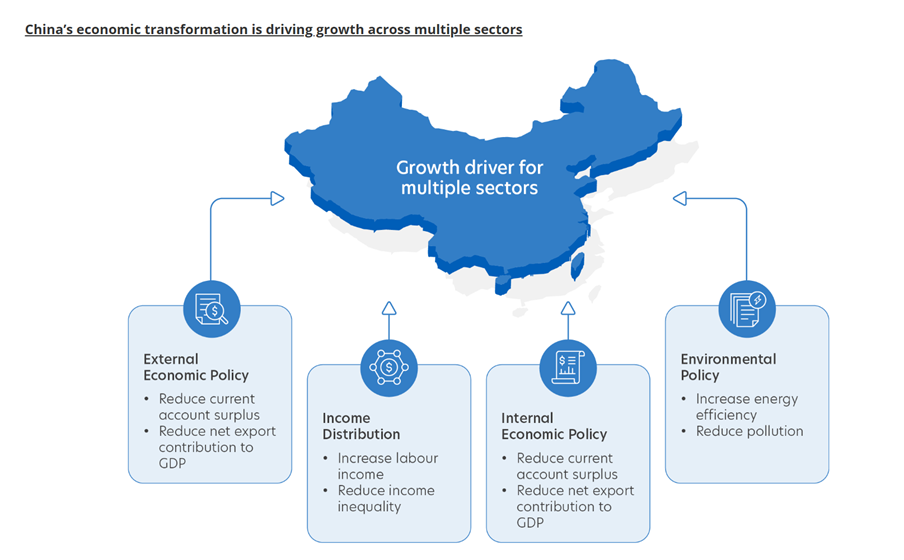

China’s economic growth has been explosive over the last decade.

Both external and internal economic policy has been targeted at long-term sustainable growth.

The policy focus has moved from old-style real-estate and heavy-infrastructure spending to boosting household consumption and scaling up next-generation industries: electric vehicles, batteries, semiconductors, AI-enabled high-tech manufacturing, and the build-out of renewable energy and ultra-high-voltage grids.

In particular, structural growth themes in the areas of healthcare, green energy, financials and consumer industry are shaping China’s future.

In the short term however, there will definitely be volatility and at the very least uncertainty about the potential trade war between the USA and China.

In the situation where the USA, being a major trading partner, imposes tariffs on all trade with China, and retaliatory tariffs ensues as a result.

No doubt this will negatively impact trade both ways.

China will likely find ways to ship goods via third party countries to reduce the tariff impact, and the tariffs may be reduced by Trump at some point.

Given how dependent China’s economy is on exports, and how they are going through a deleveraging in their real estate sector, this will likely have an impact on China’s economy.

So China stocks are cheap and uncorrelated to the rest of the world, but there definitely are risks.

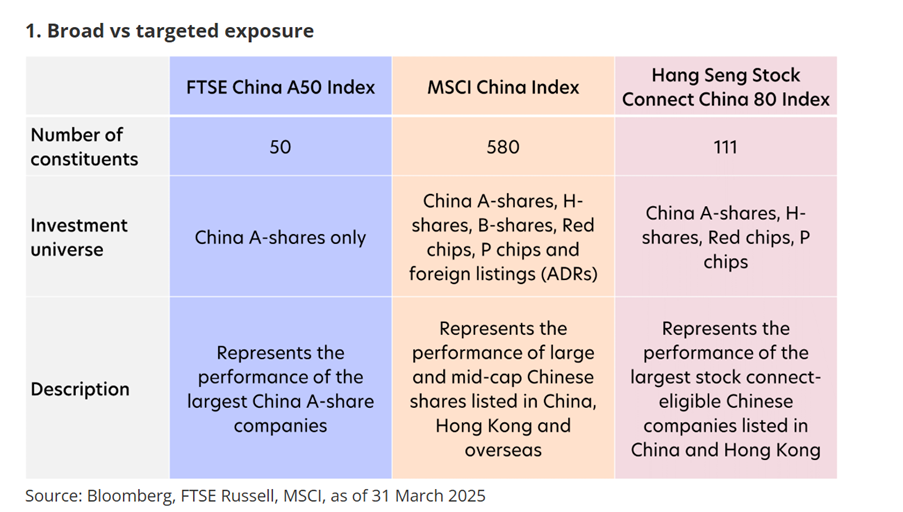

There’s a great summary from UOB Asset Management on the difference between the various China Indexes:

Of the three indices under comparison, the MSCI China Index offers the broadest exposure as it includes China shares listed on the mainland (A-shares and B-shares), in Hong Kong (H-shares, Red chips, P chips) and overseas (such as American Depository Receipts (ADRs)).

The Hang Seng Stock Connect China 80 Index is more concentrated. It is comprised of the 80-or-so largest Chinese companies listed in Hong Kong and/or mainland China that are eligible for trading under the Stock Connect scheme. Launched in 2014, Stock Connect is a mutual market access programme enabling investors either in Mainland China or Hong Kong to trade and settle shares listed on the other market via the stock exchanges and clearing houses in their home market.

The FTSE China A50 Index is solely focused on China’s 50 largest A-share companies listed in Mainland China, that is, on the Shanghai Stock Exchange (SSE) and the Shenzhen Stock Exchange (SZSE), and traded in the domestic Renminbi (RMB) currency. Of the three under comparison, this index is the most representative of China’s domestic economy and makes up about one third of the entire A-share universe by weight.

Really – I think they hit the nail on the head here.

The A50 Index gives you very targeted exposure to the China A share market (onshore), which is generally not easy to replicate as a retail investor.

The other benefit with the A50 Index – is the higher dividend yield relative to the other indexes.

UOB Asset Management further summarises the bottom line below:

- For investors with an aggressive risk appetite, the Hang Seng Stock Connect China 80 Index offers good exposure to megacap China tech stocks.

- For investors seeking to invest in a wide array of sectors and stocks ranging from mid-cap to mega-cap, and both onshore and offshore-listed securities, the MSCI China Index may be well-suited.

- Finally, investors seeking a lower-volatility exposure to the China market and healthy dividend payments may prefer the FTSE China A50 Index. The high exposure to large cap domestic companies may also offer some insulation amid the intensifying US-China trade war.

Again – I really agree with UOB AM above.

Viewed broadly, the UOBAM FTSE China A50 Index ETF gives you broad exposure to the China onshore stock market, via mainly large cap domestic markets, and with relatively high(er) dividend yield.

Definitely worth considering as an alternative to the usual MSCI China Indexes, for Singapore based investors who are looking for lower-volatility, higher dividend exposure to China.

The management fee is currently 0.45% per annum[2].

Dividends are currently at the sole discretion of the fund manager.

However, the fund intends to “make annual distributions around December each year as at such date as we may from time to time determine”[3].

UOBAM FTSE China A50 Index ETF is available for subscription with the following brokers.

Find out more here.

Disclosure: This post is sponsored by UOB Asset Management. All views and opinions expressed in this post are from Financial Horse.

The content here is for informational purposes only and should NOT be taken as legal, business, tax, or investment advice. It does NOT constitute an offer or solicitation to purchase any investment or a recommendation to buy or sell a security. In fact, the content is not directed to any investor or potential investor and may not be used to evaluate or make any investment. Do note that this is not financial advice. If you are in doubt as to the action you should take, please consult your stock broker or financial advisor. This advertisement has not been reviewed by the Monetary Authority of Singapore.

[1] FTSE, as of 31 January 2025

[2] UOB Asset Management, retrieved on 3 June 2025

[3] Distributions (in SGD) are not guaranteed. Distributions may be made out of income, capital gains and/or capital. This relates to the disclosed distribution policy as set out in the Fund’s prospectus.

I’ve been getting a lot of questions about China of late. Because of the US-China tariffs, China stocks have sold off, which presents opportunity for investors who believe in either: Plus the sell-off has made valuations more attractive than where it was at the start of the year. UOB Asset management recently launched a new

The post How to invest in China as a Singapore Investor? Is it a good time to buy China stocks? appeared first on Financial Horse.