We’ve been doing quite a few macro articles of late. So I figured let’s go back to basics this week, and address some of your burning questions. 2 questions in particular stood out: We’ll discuss KIT today. And the GBP question tomorrow. This is a modified FH Premium post written in March before the current […]

The post Will I buy Keppel Infrastructure Trust at 10% dividend yield? After the market sell-off? appeared first on Financial Horse.

We’ve been doing quite a few macro articles of late.

So I figured let’s go back to basics this week, and address some of your burning questions.

2 questions in particular stood out:

- Is Keppel Infrastructure Trust a good investment?

- Circling back on the reader’s query on how to invest in GBP

We’ll discuss KIT today.

And the GBP question tomorrow.

This is a modified FH Premium post written in March before the current market sell-off.

As I am getting many questions on Keppel Infrastructure Trust, I am making this available to all readers to keep you updated on my thinking.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

These were the questions I received from readers:

Hi FH,

I was wondering if you could provide a quick input on Keppel Infrastructure Trust’s (KIT) recent performance.

I am looking through the business’ recent performances and the numbers do not appear encouraging (with stock price now hovering at 52-week low). That said, I noted your Watchlist’s point that KIT should do well in an inflationary environment.

After reading your recent review on Keppel, I am weighing if it would be more worthwhile to invest in Keppel rather than KIT.

Thank you.

And…

For those invested or considering Keppel Infrastructure Trust. some concerns raised on their corp governance.

FH has written on KIT in the past, also had some concerns on fundraising and debt load at the time.

Mak Yuen Teen has issues with its corporate governance.

Professor MYT is the founding director of the Centre for Investor Protection. He is Professor (Practice) of Accounting at the NUS Business School, and was a former Vice Dean of the School, where he founded the first corporate governance centre in Singapore at NUS.

Here’s the report referenced for those interested: https://corporate-monitor.org/wp-content/uploads/2025/03/KIT_An-Erosion-of-Trust_25-Mar-2025.pdf

For the record, this was my initial, off the cuff reply in the private Telegram group:

Leaving aside the cg issues, KIT to me is an inflation / infra play. Short term inflation is not an issue, hence not bullish. Charts are not pretty too, so not adding until it finds a bottom.

But let’s do a deeper dive to analyse Keppel Infrastructure Trust in further detail.

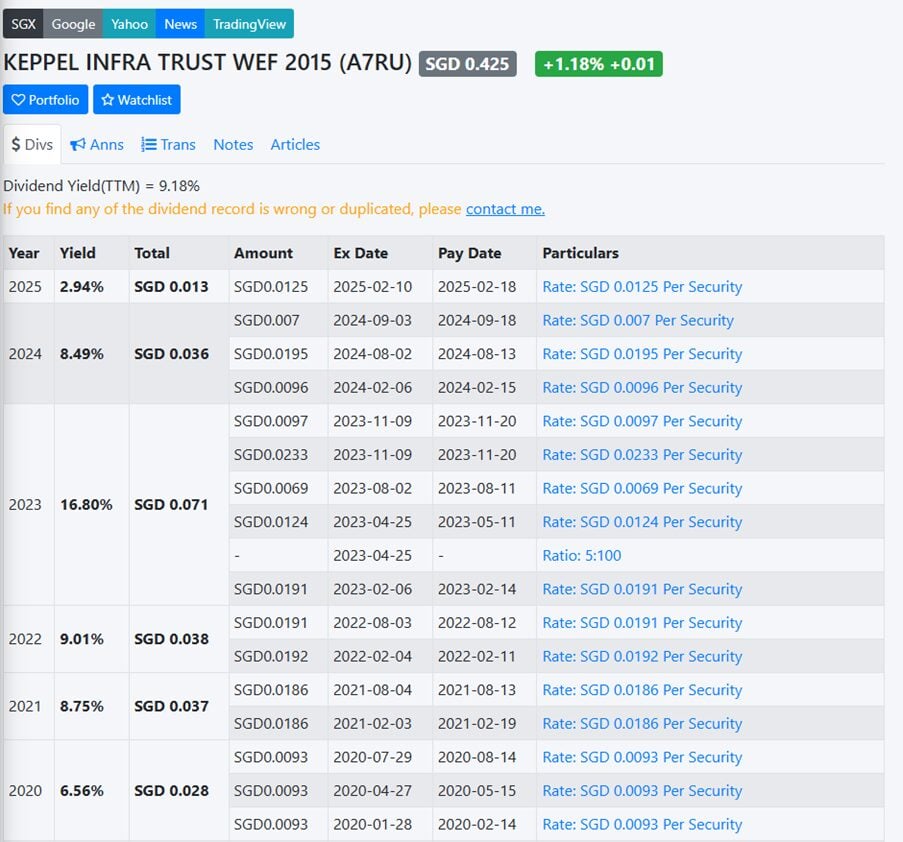

Keppel Infrastructure Trust pays a 3.9 cents trailing dividend.

Annualising that out – works out to a mind blowing 9.17% dividend yield (Note: this would be even higher today after the sell-off, as I wrote this article in March).

And if you look at the dividend track record post COVID, it hasn’t been too shabby frankly:

The chart for Keppel Infrastructure Trust is trending down and doesn’t look good.

For me personally, considering my average buy in price for Keppel Infrastructure Trust, total return including dividends is in the 40-50% range (have held this position for 2 – 3 years).

So just for me personally, I wouldn’t say it’s been a bad investment.

As long as the share price stays fairly stable / not down too much, the high dividend generates a good chunk of the total returns (a bit like the China banks for me now that I think about it).

But of course, nobody invests in a stock for the historical performance.

It’s the future performance we care about.

The Corporate Monitor report is here for those who are keen to understand the allegations.

Basically, the allegations are for lapses in corporate governance.

I don’t want to be seen supporting those allegations, so I’m not going to summarise them on the public site, and you can read the report if you want to understand more.

Let me share my personal views across 3 areas:

- Corporate Governance issues flagged

- Acquisitions made by Keppel Infrastructure Trust

- Financial Results of Keppel Infrastructure Trust

Follow Financial Horse to avoid missing any post!

As investors in public stocks, most of us may not care so much about corporate governance, but we definitely care insofar as will it impact stock price.

The tricky part is knowing whether the issues are material enough to impact the stock price.

This is something investors have to weigh.

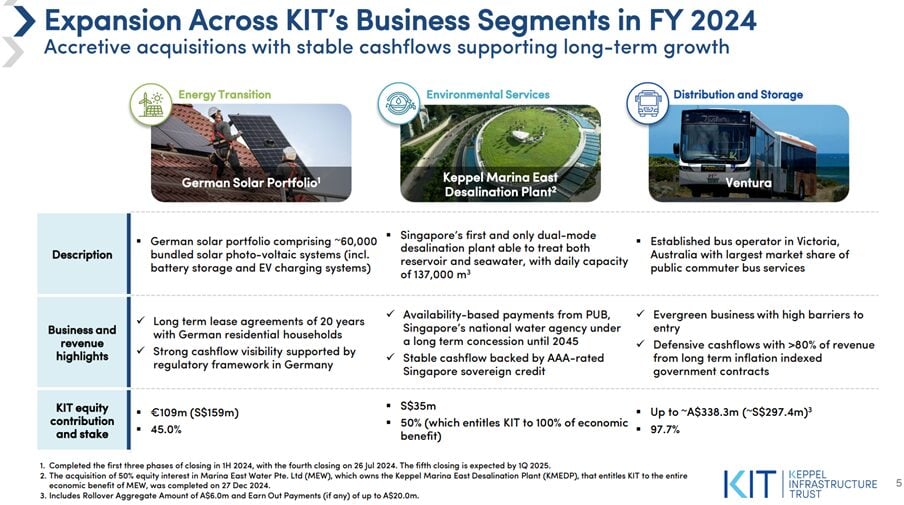

Many stock holders have raised concerns about Keppel Infrastructure Trust’s acquisition strategy.

Acquisition of a bus company in Australia (Ventura) – questions have been raised.

Buying a German solar portfolio, a Keppel Marina East desalination plant – perhaps more aligned to infrastructure play.

While I am inclined to give management a chance to prove that they do have a solid plan, as the saying goes – Trust, but verify.

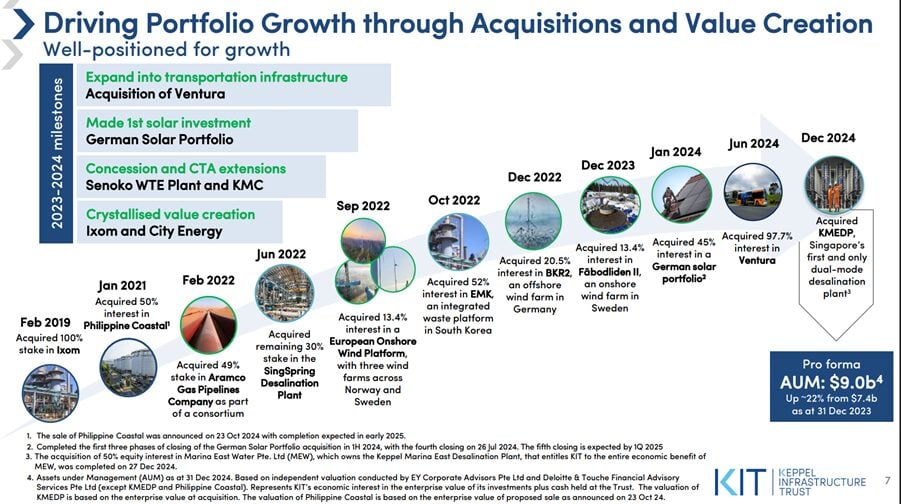

If you look at the acquisition track record.

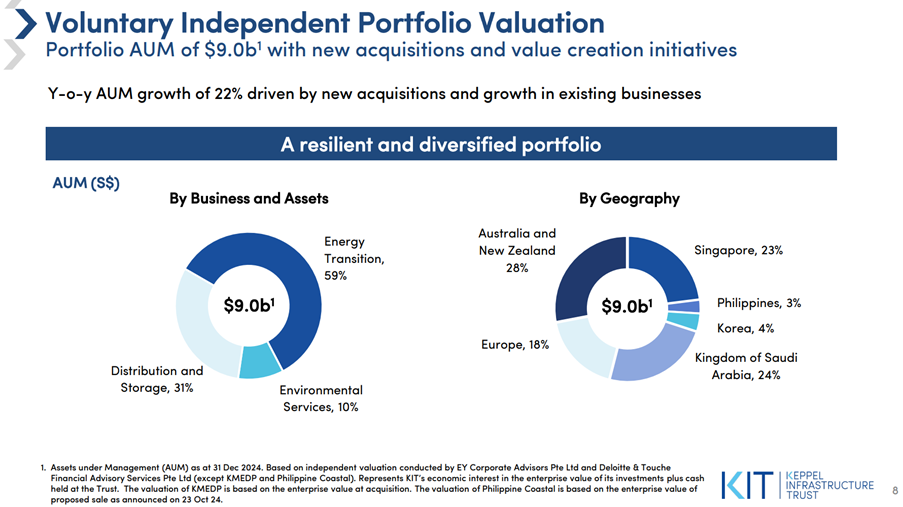

It’s been a flurry of acquisitions post-COVID, a lot of them not located in Singapore.

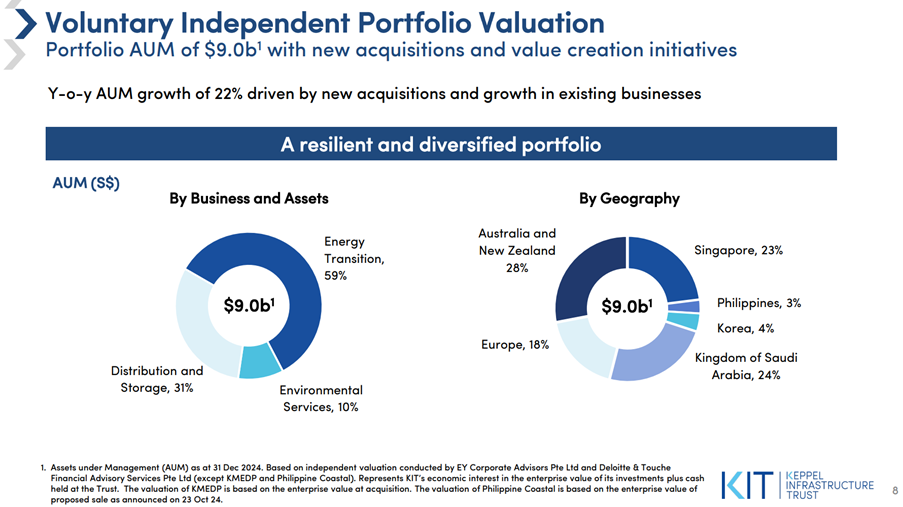

Keppel Infrastructure Trust today – only 23% of the portfolio is Singapore infrastructure assets.

I guess my point is this.

Keppel Infrastructure Trust holding Singapore electricity, water assets – something investors have come to expect and support.

Keppel Infrastructure Trust buying overseas infrastructure assets – questions may arise regarding the expertise required to curate the right mix of assets, as well as to run these assets all over the world.

Beyond the corporate governance, this is probably my biggest concern for Keppel Infrastructure Trust.

The investment has been performing well for me in my personal context.

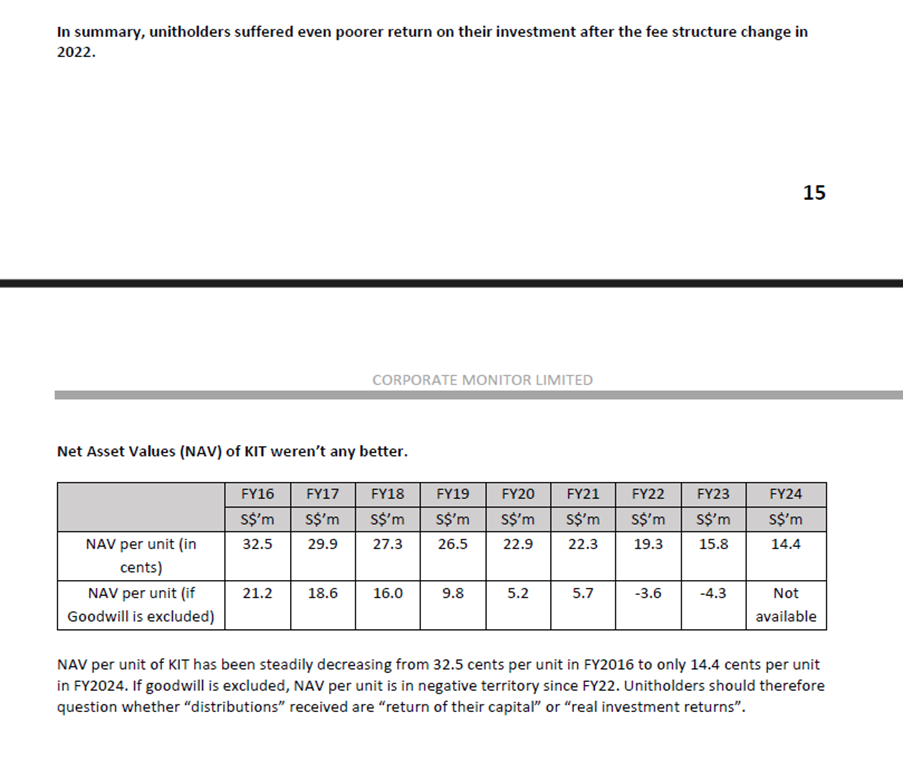

But as the Corporate Monitor report shows, unitholders who invested in KIT 10 years ago would actually be underwater.

In some ways this goes back to the same corporate governance point flagged by Corporate Monitor above.

I frankly don’t care about corporate governance if the share price continues to do well.

But what investors may be worried about is whether corporate governance issues will affect decision making to the extent it has implications for future share price performance.

For what it’s worth, financial results for Keppel Infrastructure Trust are not as straightforward to read as a REIT.

You need to think of Keppel Infrastructure Trust more as an operating business than a landlord collecting rent.

So the earnings are lumpy, and fluctuate over time.

My general view is that the financial results are decent, but not fantastic.

The time they were actually fantastic, was in the 2022-2023 period when inflation was raging.

And really, that’s how I see Keppel Infrastructure Trust.

This is an infrastructure play, that does well when inflation is high.

When inflation is muted (and projected to stay under control) like right now, you would expect less stellar financial results as we are seeing.

After looking at the financial results and the Corporate Monitor report.

I think my view stays pretty much the same:

Leaving aside the cg issues, KIT to me is an inflation / infra play. Short term inflation is not an issue, hence not bullish. Charts are not pretty too, so not adding until it finds a bottom.

From a technical analysis perspective – the stock is trending down, it has broken key supports, and it’s sitting below the 50, 150, and 200 day moving average.

That’s as bad as it gets and I don’t see why I would want to bottom fish for a stock like that right now.

And from a fundamental perspective, this is an infrastructure play, that does well when inflation is high.

But with the US in deficit cutting mode, and concerns for growth tilted towards the downside, I don’t really see inflation being a huge concern near term.

Would it be better to just buy a plain vanilla REIT, which could outperform in a lower interest rate climate?

Big picture wise, I do have my concerns that with such a global infrastructure portfolio – whether Keppel Infrastructure Trust will be able to run this portfolio to face whatever challenges are to come.

What do you guys think? Let me know in the comments below.

This is a modified FH Premium post written in March before the current market sell-off.

As I am getting many questions on Keppel Infrastructure Trust, I am making this available to all readers to keep you updated on my thinking.

For my latest macro views, and what I am buying/selling, do consider subscribing for FH Premium.

You will also get access to my latest macro views, full stock / REIT watchlist, and personal portfolio (updated weekly).

We’ve been doing quite a few macro articles of late. So I figured let’s go back to basics this week, and address some of your burning questions. 2 questions in particular stood out: We’ll discuss KIT today. And the GBP question tomorrow. This is a modified FH Premium post written in March before the current

The post Will I buy Keppel Infrastructure Trust at 10% dividend yield? After the market sell-off? appeared first on Financial Horse.