So I received this email from SGX setting out the “Top 5 Most Net Bought Singapore Stocks by Institutions in 2024”. Of course I expected DBS, OCBC and UOB to be at the top of the list. Imagine my surprise when I opened it up – to find that the number 1 name was actually… […]

The post Why I may buy Singtel at 5.0% dividend yield? Most bought Singapore Stock by Institutions in 2024? appeared first on Financial Horse.

So I received this email from SGX setting out the “Top 5 Most Net Bought Singapore Stocks by Institutions in 2024”.

Of course I expected DBS, OCBC and UOB to be at the top of the list.

Imagine my surprise when I opened it up – to find that the number 1 name was actually…

Singtel

At $825 million in net inflow, it beat UOB’s inflow by almost $300 million (DBS doesn’t even feature on the top 5 list).

Regular readers know that I looked at Singtel about half a year ago – and my conclusion was that I really liked what I saw.

I liked the dividend increase, I liked the new strategic transformation of the company, and I liked how management was executing.

What I didn’t like so much was the chart – which was going parabolic at the time and likely susceptible to a pullback.

Well – half a year has passed since my original article.

Today, Singtel still sits at about 3.10ish, roughly the same price as where it was 6 months ago.

But – the chart looks very different.

Because I now have the pullback I was waiting for, and price is sitting right on the 50 day moving average.

All while the recent decline comes on low volume.

It’s interesting enough that if you think the fundamentals for Singtel are bullish, this might actually be a decent spot to add if the technicals hold up.

For that we’ll need to dive into the fundamental analysis.

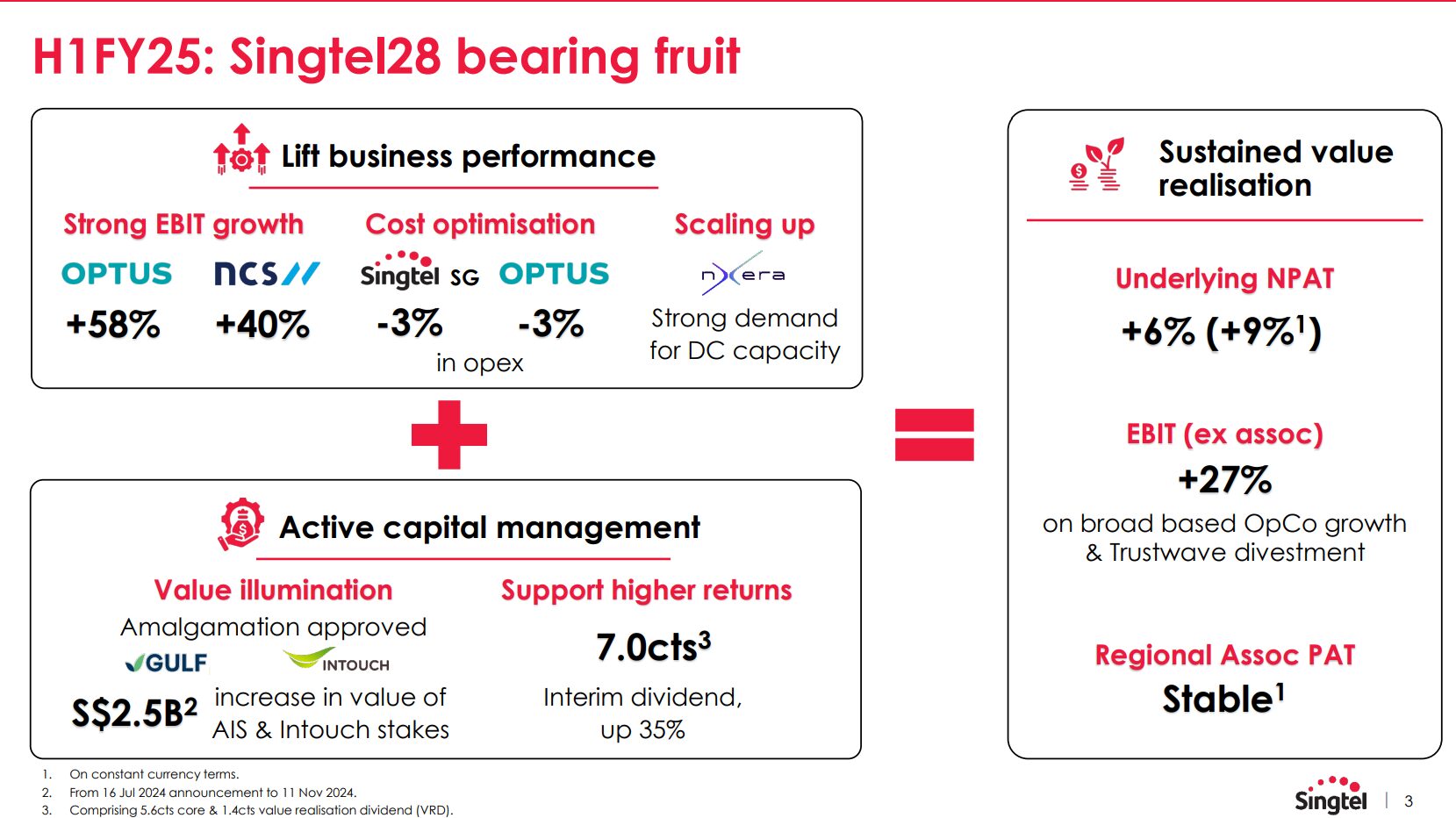

Singtel today is broadly split into 2 parts:

- The core telco business – Optus and Singtel

- The “Growth” business – NCS and Digital Infrastructure (nxera)

You can see the high level numbers below.

Generally it paints a picture of the core telco business staying resilient and stemming the bleed that we saw previously.

While the “Growth” business looks to be delivering decently on growth so far.

That said, for now at least, Singtel remains very much a telco company.

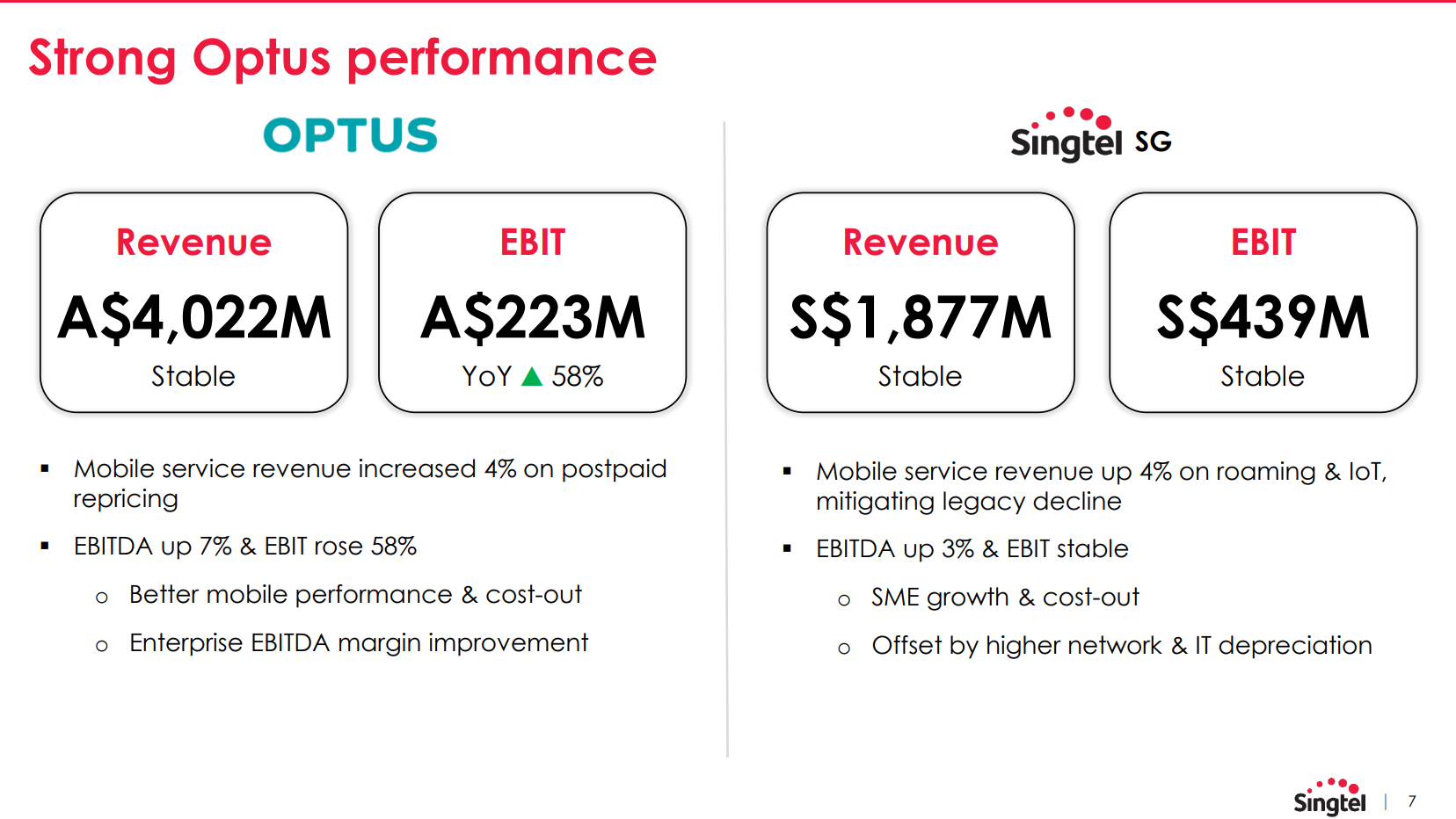

The bulk of their earnings continue to come from the Australian Telco Optus, and the Singtel telco (Singtel).

So you can say all you want about growth from NCS and AI data centres, but if you want to buy a position in Singtel you do need to have a view on the Telco business as well.

For what it’s worth, it looks like the worst is over in the Telco price wars in Singapore.

Remember back when there was all that talk about the entry of a fourth Telco player into Singapore, and the entry of MVNOs and all that?

Well it’s fairly clear that this market is not big enough for that many players.

So after a lengthy period of consolidation, and huge losses for Telco players, that saga seems to be over (for now).

Which is why we see stable revenue and EBIT for Singtel’s core Singapore business.

And for now at least, let’s hope it stays that way.

Optus on the other hand looks to be executing well, with a remarkable 58% growth in EBIT.

This is largely due to a combination of higher revenue, and lower operating expenses.

On face value – this looks very strong.

That being said, I am less familiar with the Australian Telco market, so if anyone has valuable insights please do not hesitate to share.

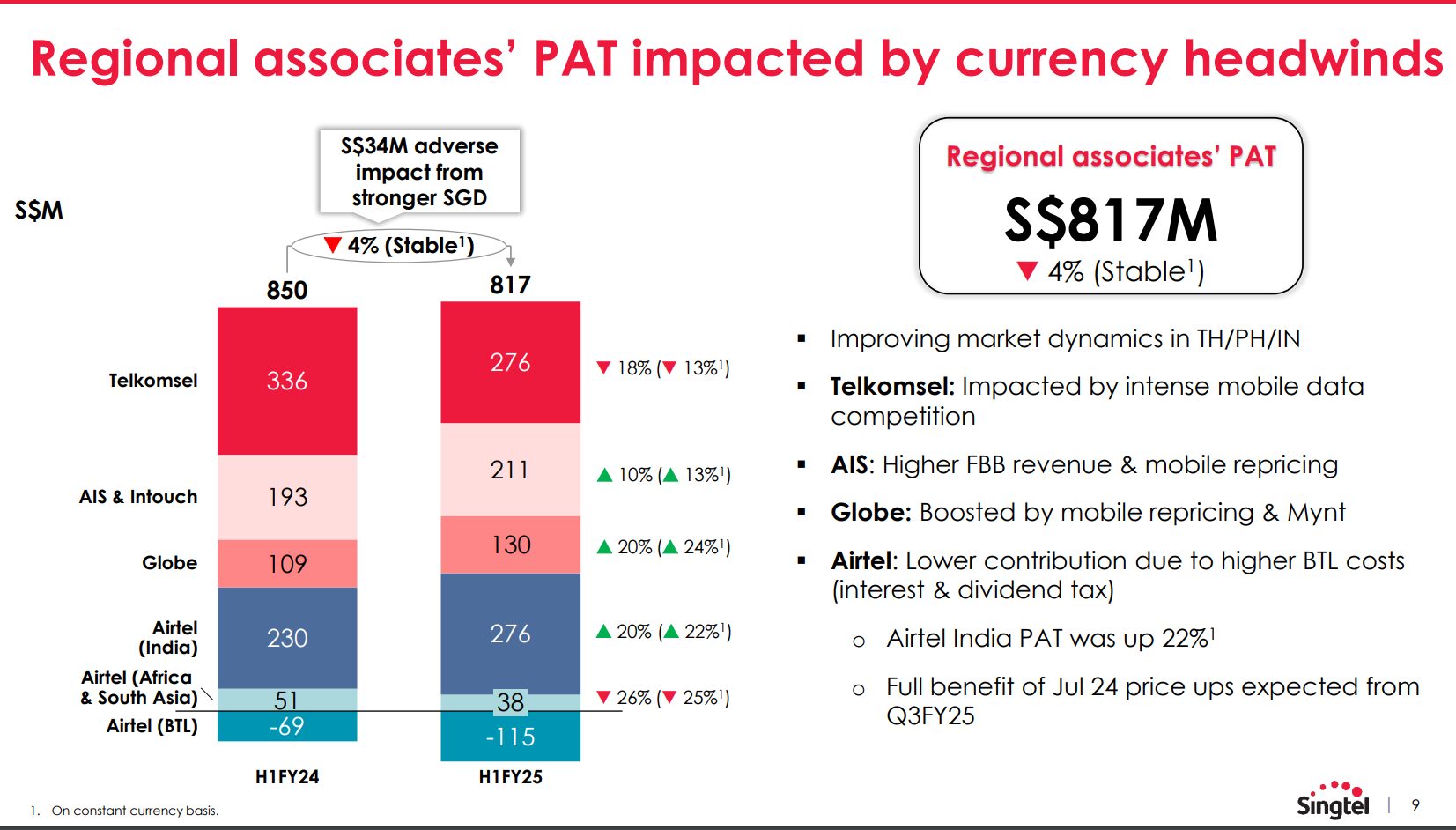

Meanwhile the performance from the regional associates is generally flattish when aggregated together.

If you dive into the numbers, Telkomsel (Indonesia Telco) in particular has been performing especially poorly, and the official reason is “Impacted by intense mobile data competition”.

This is not a good sign, as it looks like the Indonesia market is going through a period of intense competition, and we all know when that happens it takes years to play out (see what happened in Singapore).

The good news though, is that the other associates like AIS (Thailand), Globe (Philippines) and Airtel (India) are doing well, so when aggregated together it produces flat earnings.

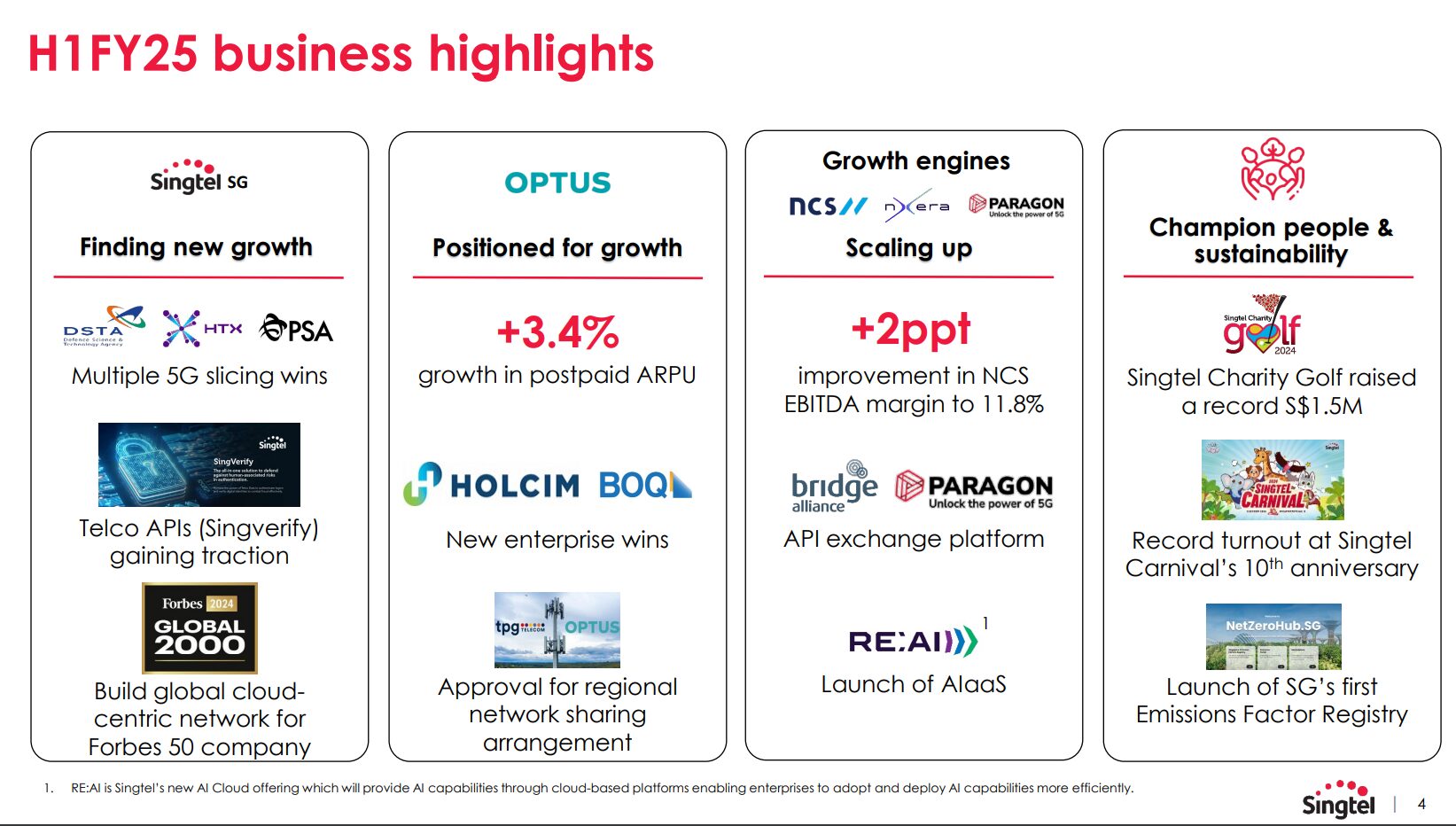

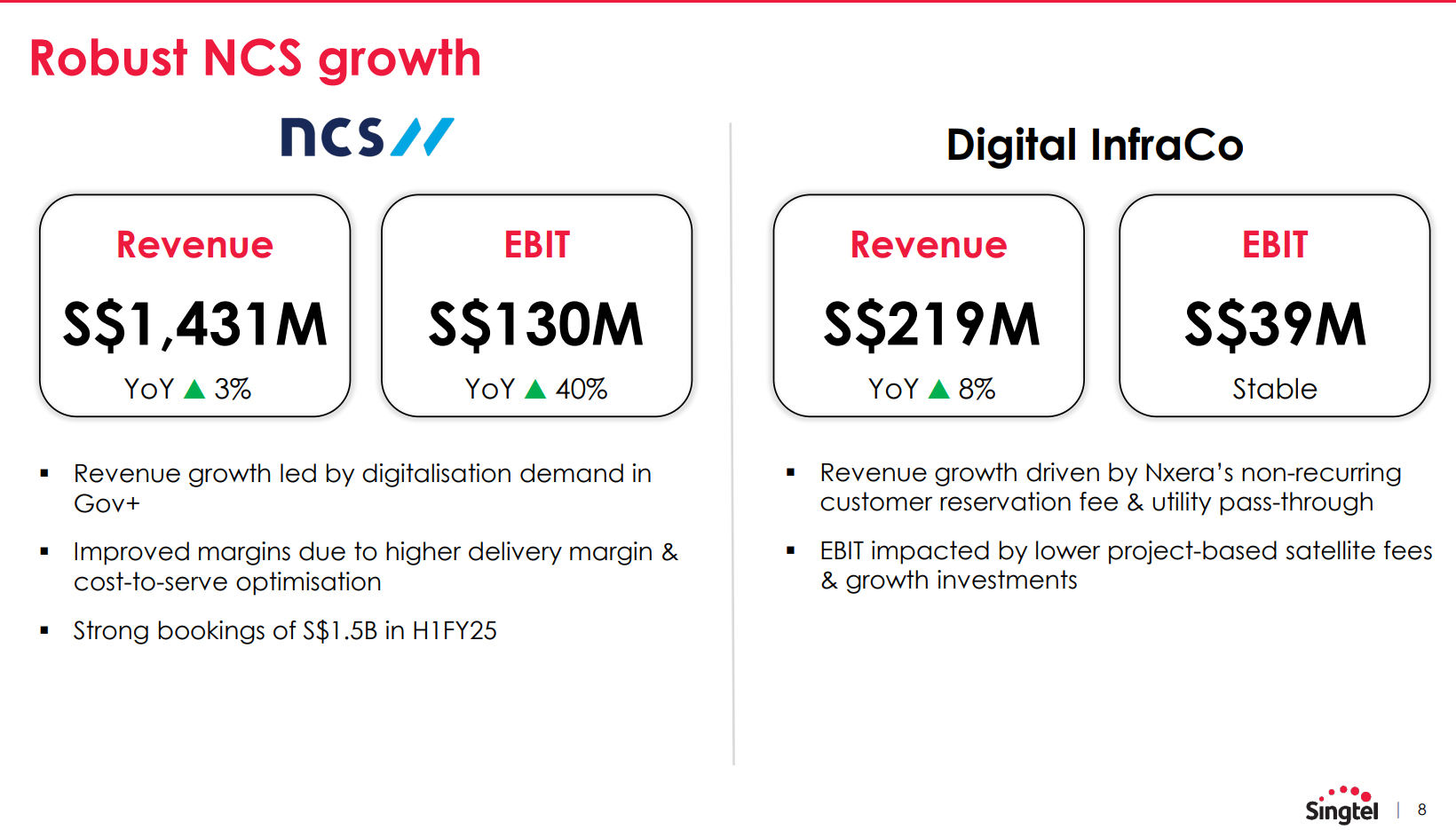

Singtel’s NCS is a technology services company that provides digital and IT solutions to government and institutional companies.

Growth has been very strong with a 40% increase in EBIT.

And $1.5 billion in bookings in H1 FY25.

This corroborates what I’ve been hearing on the street – which is that NCS has been performing very well of late due to increased digitalisation demand from governments and corporates.

Meanwhile Digital Infrastructure (Nxera) is the new business line, which focusses on the “sexy” stuff like AI data centres.

Both are very promising.

But that being said, at $170 million combined EBIT, the still make up less than 30% of the EBIT from the core Telco business.

Which is why I said that yes while you can buy Singtel because you like the new “growth” sectors, don’t forget that for now the bulk of the profits continue to come from the traditional Telco business.

So if Telco underperforms that’s a big chunk of the Singtel business that will still underperform.

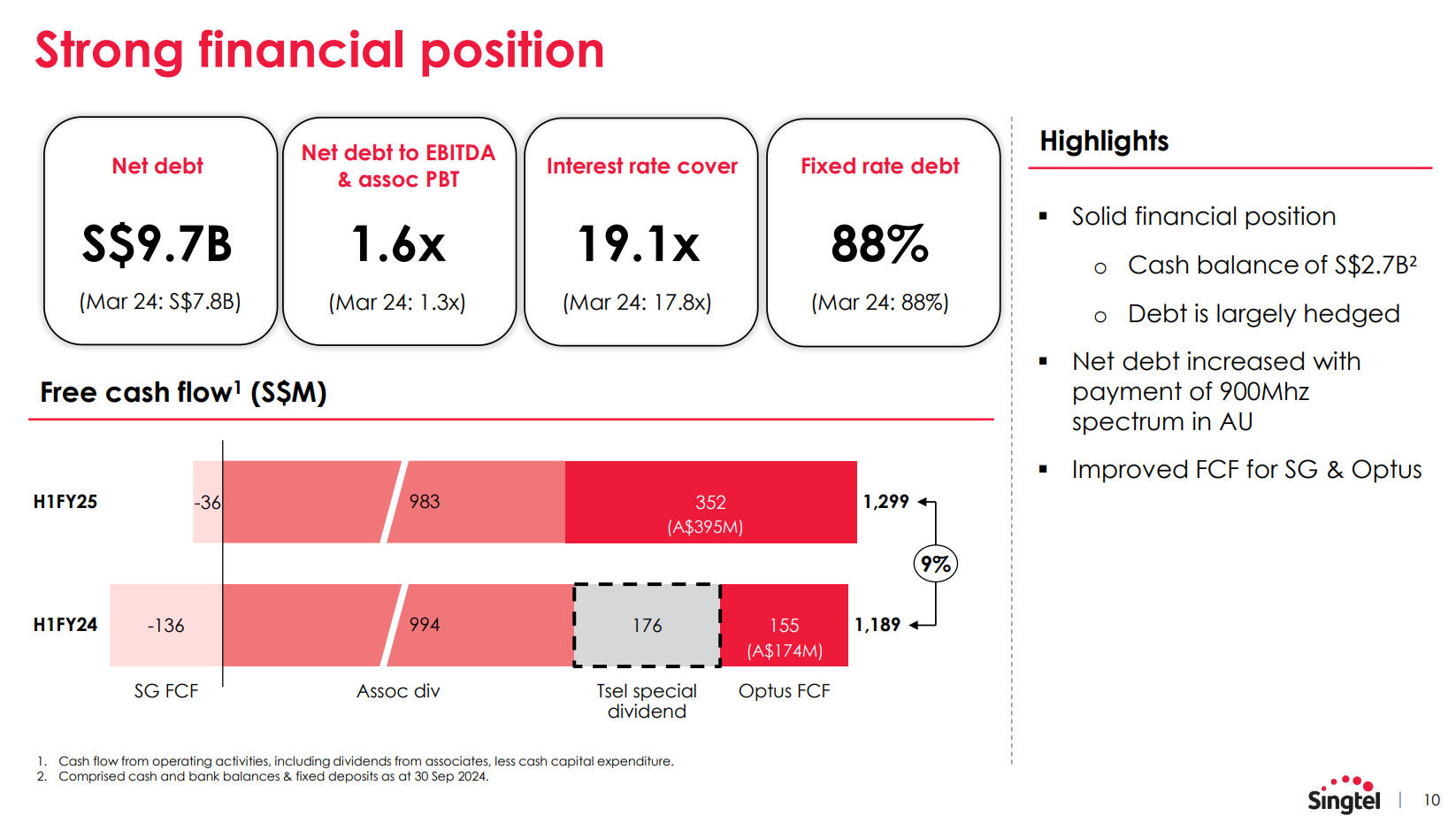

For what it’s worth, Singtel has a fairly strong balance sheet.

Net debt to EBITDA is a very decent 1.6x.

The way I see balance sheet though, is that it buys you time.

If you have a strong balance sheet, mistakes becomes more forgiving.

If you have a weak balance sheet, small mistakes can become very punishing.

But don’t kid yourself – nobody invests in a company on the basis of a strong balance sheet.

The balance sheet is there to buy management time to deliver on business growth.

So the bulk of the analysis should focus on the above – enough said.

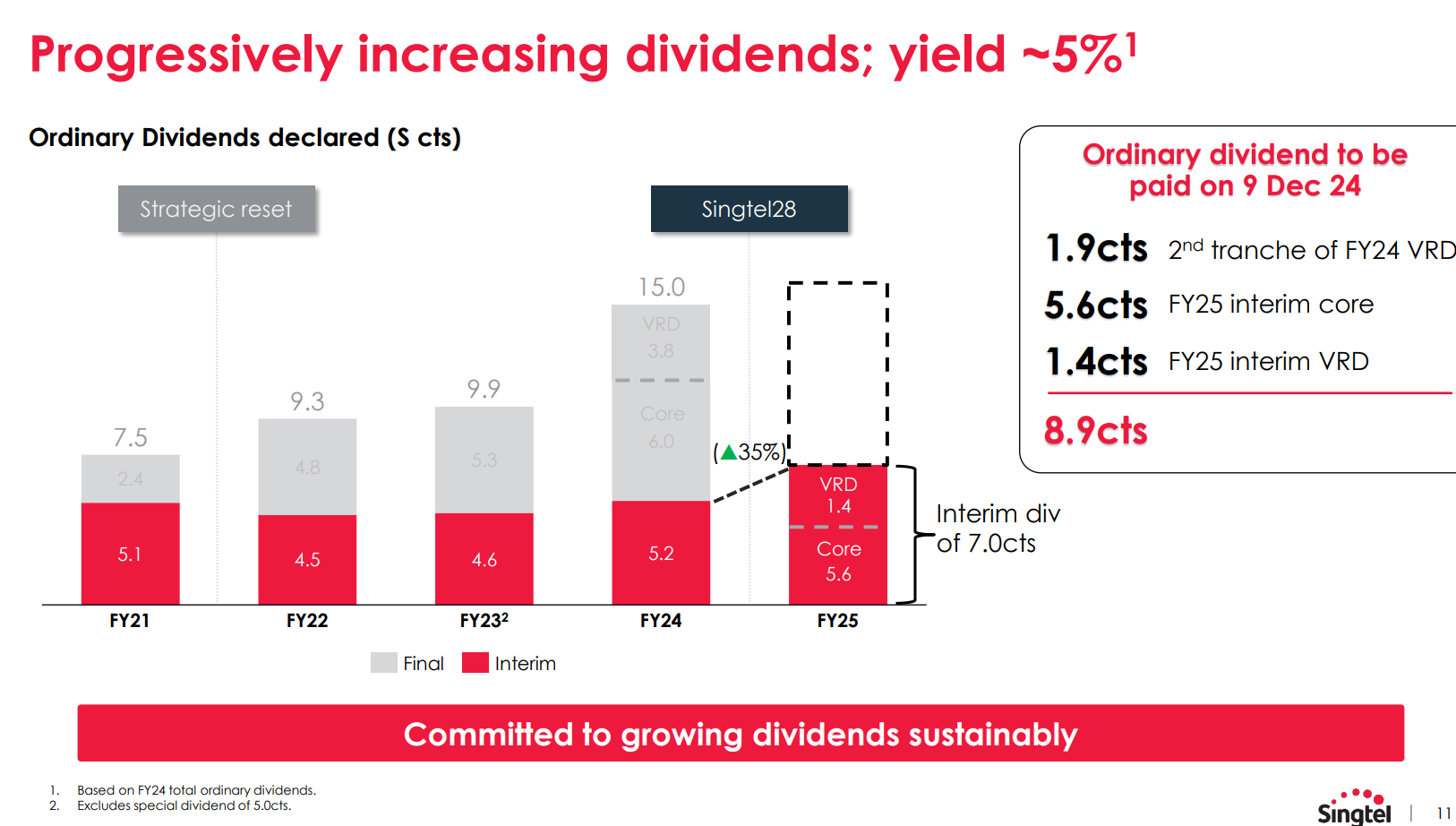

At this price, assuming the value realisation dividend continues (and all signs from management suggest that it will for now).

You’re looking at a 4.8% dividend yield at latest price.

That’s actually in line with the dividend yield from DBS, UOB and OCBC bank.

So not too shabby.

Follow Financial Horse to avoid missing any post!

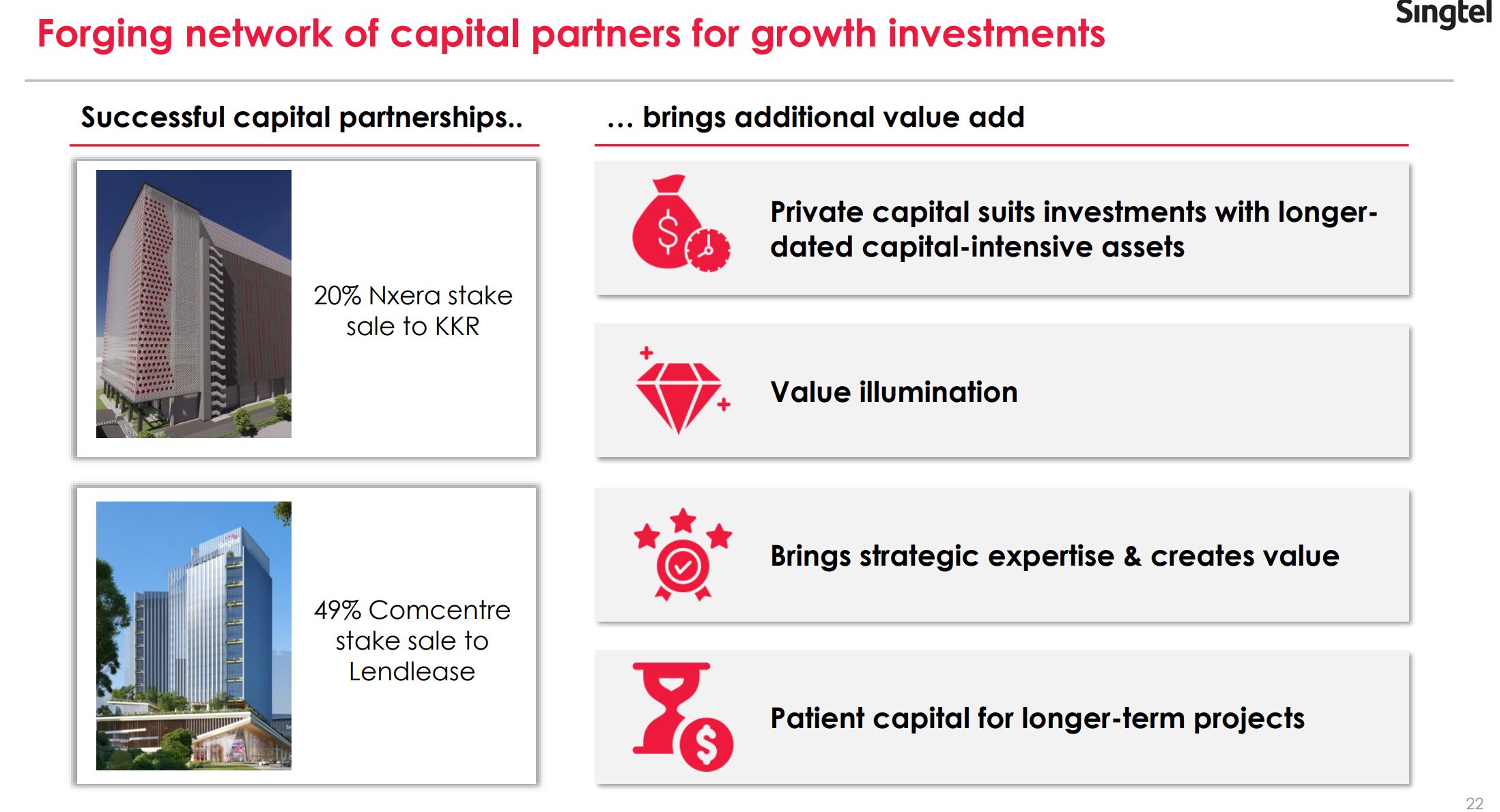

In my previous article on Singtel, I talked about 3 key factors that drove the 30%+ surge in share price from 2.3 to 3.1.

Broadly they are:

- Dividend increase – Value Realisation Dividend

- Successful capital recycling – selling lossmaking assets like Trustwave and Amobee, selling 49% of Comcentre to Lendlease

- Focussing on AI growth – pivoting into the AI growth story with a 20% Nxera stake sale to KKR

The third one is particular is worth elaborating on, and this was what I wrote back in 2024:

“Singtel’s Data Centre Business – 20% sale to KKR at $1.1 billion

Per reporting from Reuters – “New York-based KKR bought a 20% stake in SingTel’s regional data centre business last year for S$1.1 billion ($816 million)”.

Now Singtel’s data centre business is still in growth phase and not a mature business.

A 20% stake at $1.1 billion would value the full data centre business at $5.5 billion.

That’s pretty generous, which indicates a lot of the valuation was “brought forward” from future revenues.

So this is a good move by Singtel to realise value for shareholders, in that it (a) brings forward future revenues, and (b) signals to the market that an established player like KKR is willing to value Singtel’s nascent data centre business at a $5.5 billion valuation.

Very well done.”

Singtel’s Nxera has also been in the news for building a AI data centre campus in Johor, all very good news you want to see as an investor (given the tailwinds for AI).

So yes… the strategic transformation is impressive and all.

But why has share price been stuck at 3.10 for the past 6 months or so?

I guess if you really think about it – most of the low hanging fruit has been plucked.

Selling the loss making assets, unlocking value in real estate, selling a stake in the nascent data centre business, upping the dividend.

Those were the low hanging fruit.

For the next leg up – the market needs to see Singtel deliver.

Deliver in the form of higher operational earnings.

And I suppose, that is where the rubber hits the road.

Will Singtel be able to deliver?

As always – we discuss a lot of points above, but at the end of the day, we need a conclusion.

And you know what?

I actually kinda like Singtel as a stock.

What’s more – the charts look very interesting to me.

We had a large runup on high volume.

Then we had a lengthy 6 month period of consolidation (on increasingly low volume).

And price is now sitting somewhere around the 50 day moving average.

If you just showed me this chart (without telling me it was Singtel), I would say that hey if this stock breaks out it could really go a lot higher.

But technical analysis aside, what’s my take on the fundamental analysis of Singtel?

Bottom line to me – Singtel today is still first and foremost a Telco business.

If the Core Telco business underperforms, it doesn’t matter how well the growth sectors of NCS or Nxera do, the stock is still going down.

The good news seems to be the for the core Telco business, the worst seems to be over (for now).

Singapore and Australia look to be doing fine, and most of the regional associates (with the exception of Indonesia) are doing okayish.

As long as the core Telco business remains stable – then it allows the upside from NCS and Nxera to come in.

And I’m actually pretty bullish on that front.

There’s a lot of structural growth factors in both sectors (AI and enterprise software).

Sometimes you just need to be in the right place at the right time, and ride the growth.

And with the Temasek backing and Singtel brand name, I could actually see Singtel being able to execute on both fronts.

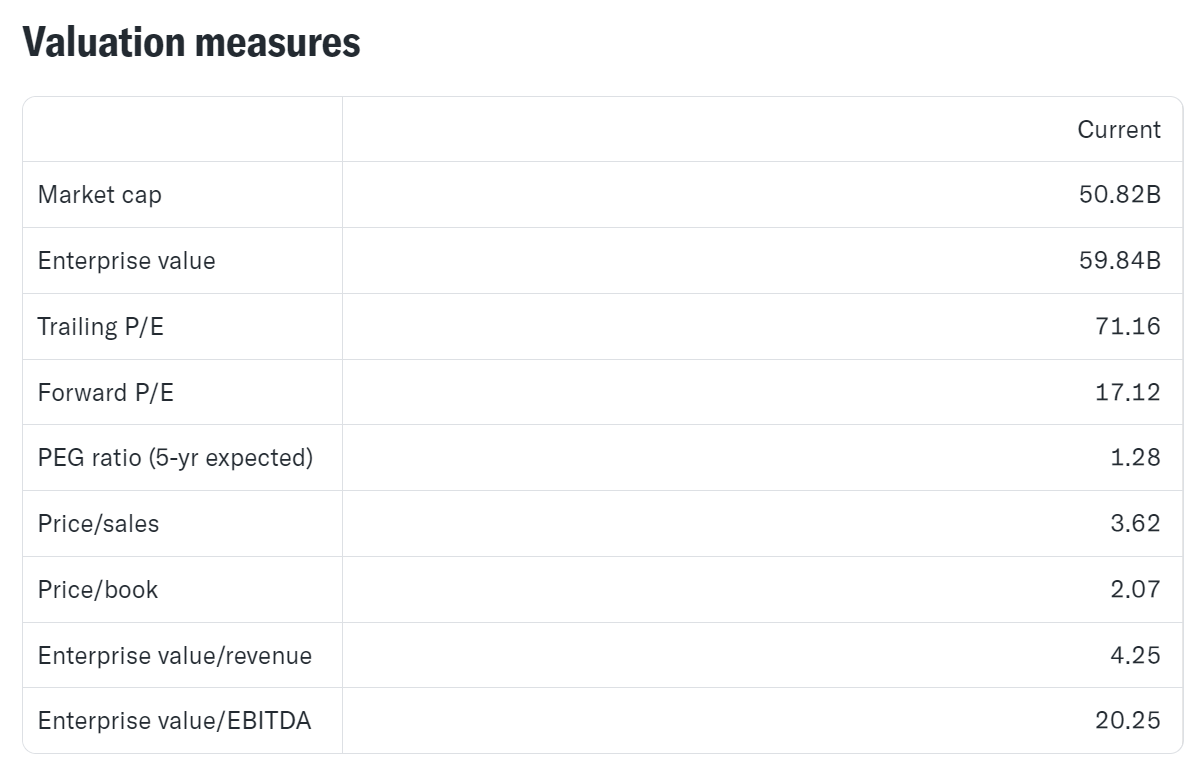

Valuations are mixed.

Forward P/E is 17x, but given this is a mix of old school telco business and nascent new world AI / enterprise software, I would say that is fair value at best.

I know the biggest question from readers is that why buy Singtel?

Why not just buy DBS Bank or CICT – both paying approximately similar 5% dividend yields?

I would say diversification comes to mind as a big one.

Both Banks and REITs have huge exposure to interest rates, whereas Singtel very much less so.

So if your portfolio today is pure Banks and REITs, there’s powerful diversification benefits from adding a non-bank non-REIT counter in.

And as shared above, there are reasons to like Singtel from a single stock perspective as well (bottom up analysis).

In any case, you can see my full stock / REIT watchlist on FH Premium, setting out the stocks and REITs I am monitoring closely and may add. I will be updating the watchlist this weekend as well.

For what it’s worth, I haven’t made up my mind on this one.

Which is why the article is titled I may buy Singtel, and not I will buy Singtel.

Regular readers know that while I have my views, I’m not afraid to change them on a dime if the facts change.

I’ll monitor the price the next few weeks, and who knows I may or may not buy a position.

As always – I’ll share latest updates on FH Premium as and when I do buy a position (or change my mind).

This post is written on 24 Jan 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

So I received this email from SGX setting out the “Top 5 Most Net Bought Singapore Stocks by Institutions in 2024”. Of course I expected DBS, OCBC and UOB to be at the top of the list. Imagine my surprise when I opened it up – to find that the number 1 name was actually…

The post Why I may buy Singtel at 5.0% dividend yield? Most bought Singapore Stock by Institutions in 2024? appeared first on Financial Horse.