A week or two back I shared my views on REITs in 2025. And I know a lot of you have been asking. So let me share my views on Singapore banks as well. I mean if you really think about it, on the SGX there’s really only REITs and Bank stocks to buy. So […]

The post Will I buy more DBS Bank stock at a 5.0% dividend yield? Are Singapore Bank stocks still a good buy? appeared first on Financial Horse.

A week or two back I shared my views on REITs in 2025.

And I know a lot of you have been asking.

So let me share my views on Singapore banks as well.

I mean if you really think about it, on the SGX there’s really only REITs and Bank stocks to buy.

So it’s worth taking some time out to think through how both may perform in 2025.

I’ll try and focus on DBS Bank specifically in this article, but the analysis can be applied more generally to OCBC Bank and UOB Bank as well.

For the record – DBS Bank’s share price was up 46% last year.

This is excluding dividends, so throw in the 6%ish dividend yield and you’re looking at a 50% total return for DBS Bank in 2025.

Pretty unbelievable stuff – that you could literally buy a boring blue chip stock like DBS Bank and make 50% in a year.

But of course, this begs the next question.

If DBS Bank delivered a total return of 50% in 2025.

What’s the likelihood that DBS Bank will deliver another total return of 50% in 2025?

If this were a growth stock like NVIDIA okay maybe I get the argument, but a real world value stock like DBS Bank?

What’s the probability of 2 consecutive years of outsized returns?

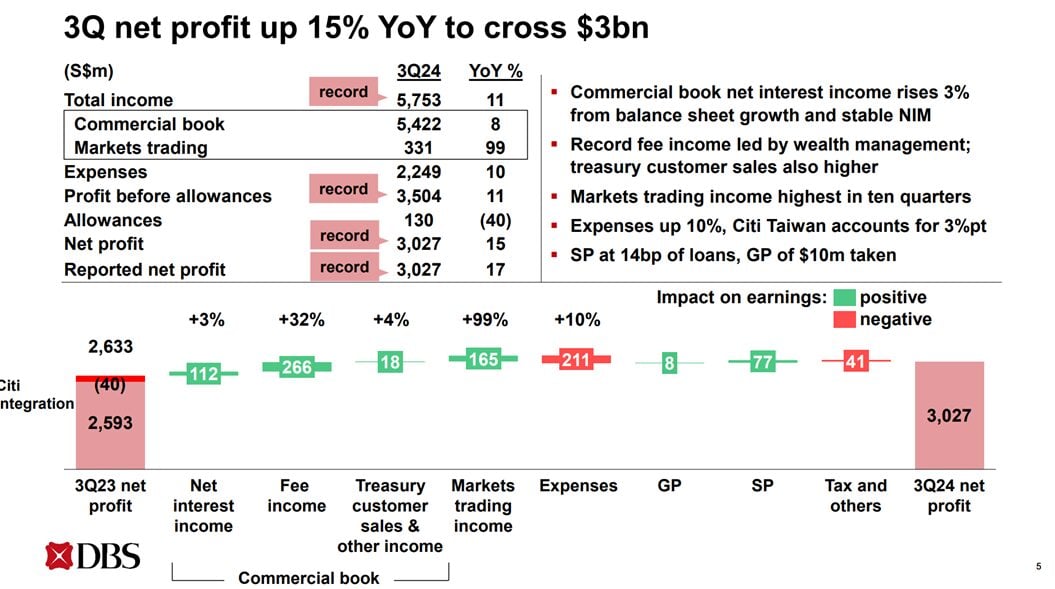

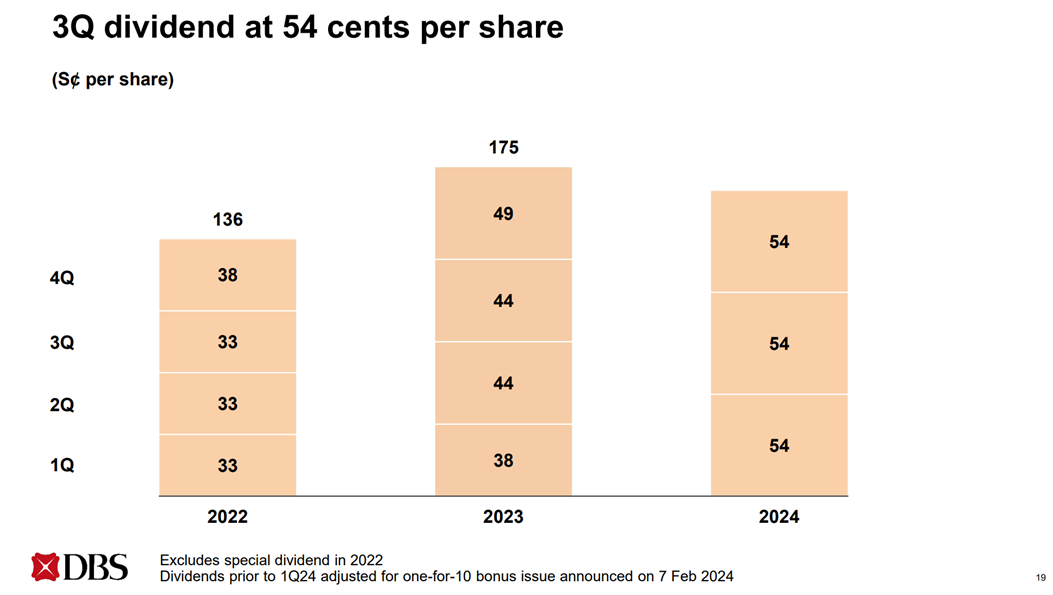

For what it’s worth, the latest quarterly financial results are stellar.

Net profit is up 15% year on year.

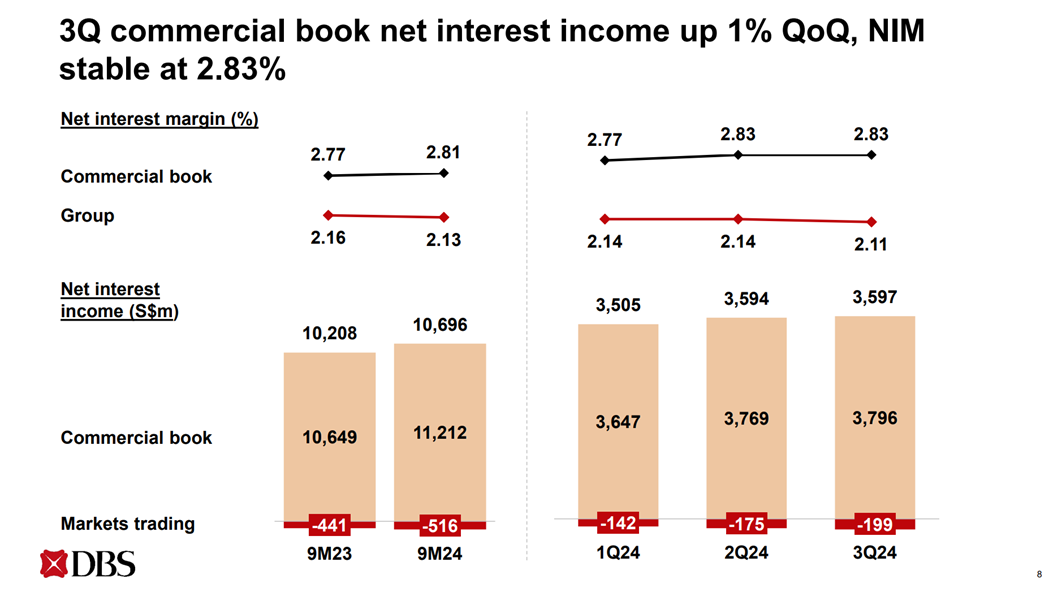

Net interest income and net interest margin is flattish, which is okay given the lower interest rate environment.

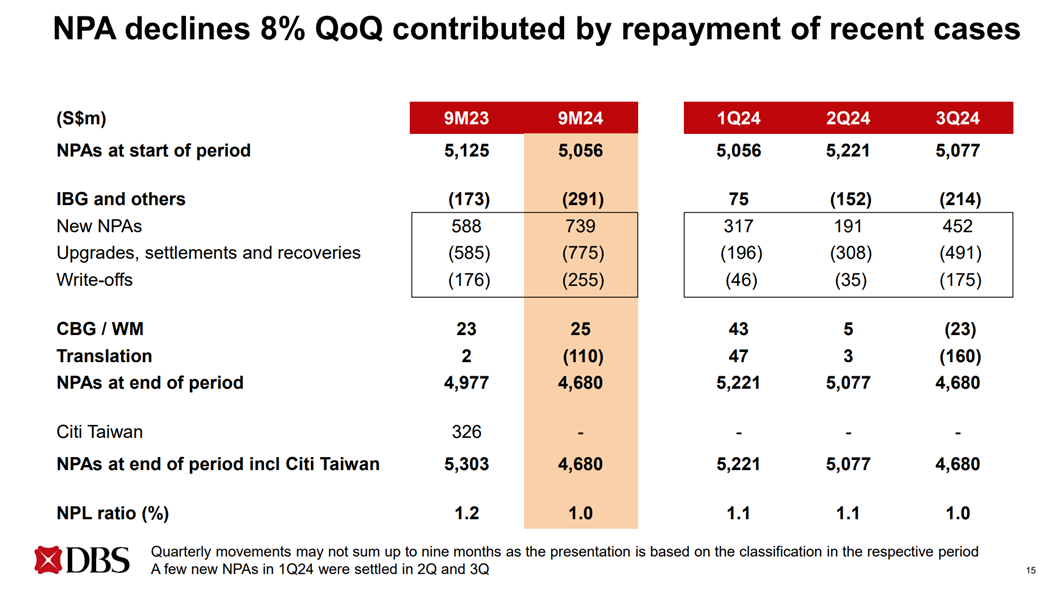

With a resilient South East Asia economy (so far at least) non performing loans remains very low, and is actually down on a year on year basis.

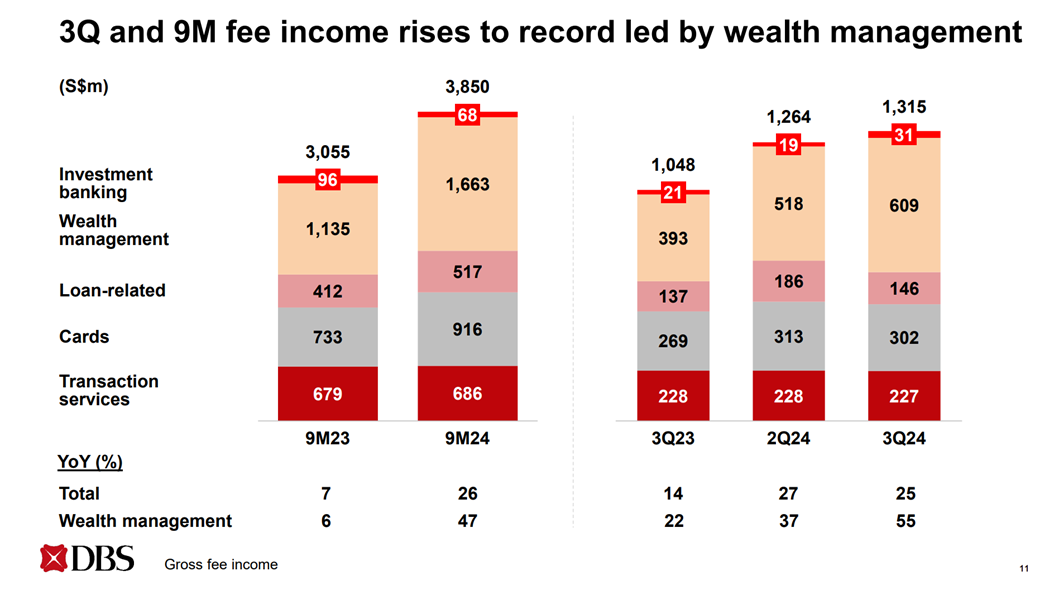

Meanwhile fee income rose to record highs led by wealth management, which is similar to what we’re seeing from OCBC as well (very strong wealth management results).

But c’mon.

You don’t need me to tell you that DBS Bank’s financial results are superb, and that by all accounts the bank is firing on all cylinders.

And for what it’s worth – that’s not what drove the recent big move in DBS’s share price.

If you look at the chart below, you’ll realise that a big move in DBS’s share price came in early Nov – right after the Trump win.

Pull up the charts for UOB / OCBC and you’ll see a similar story.

I suppose it came down to 2 factors:

- Expectations of a stronger US economy (because you know… Trump)

- Stronger US economy = steeper yield curve which is good for banks

And given Singapore’s interest rates track US interest rate closely (because of the impossible trinity – MAS cannot control interest rates because it controls FX and has free movement of capital).

A steeper yield curve for the US, translates into a steeper yield curve for Singapore – and therefore good for the banks.

This was why I added to my bank stock positions in the days leading up to the Nov elections (in anticipation of a Trump win), and on the day that Trump won I added further to bank stocks as well (okay to be fair I also added to crypto / tech as alternative Trump plays).

It’s probably worth discussing the macro outlook under Trump at this point.

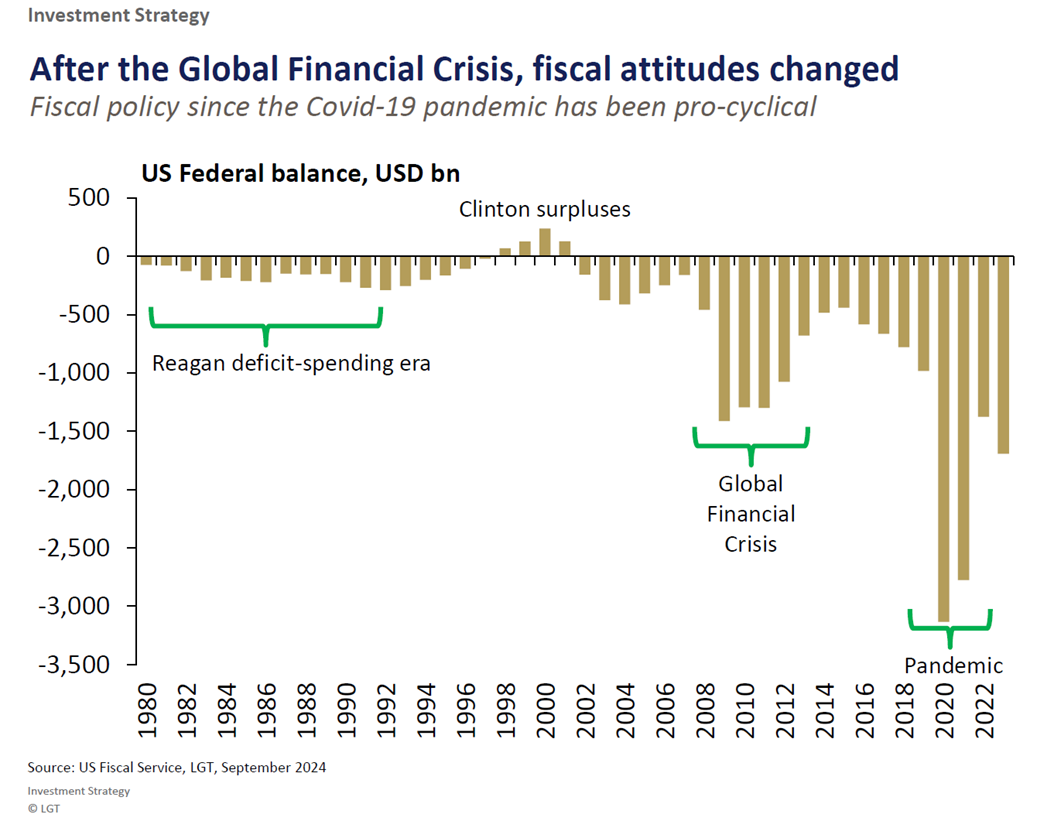

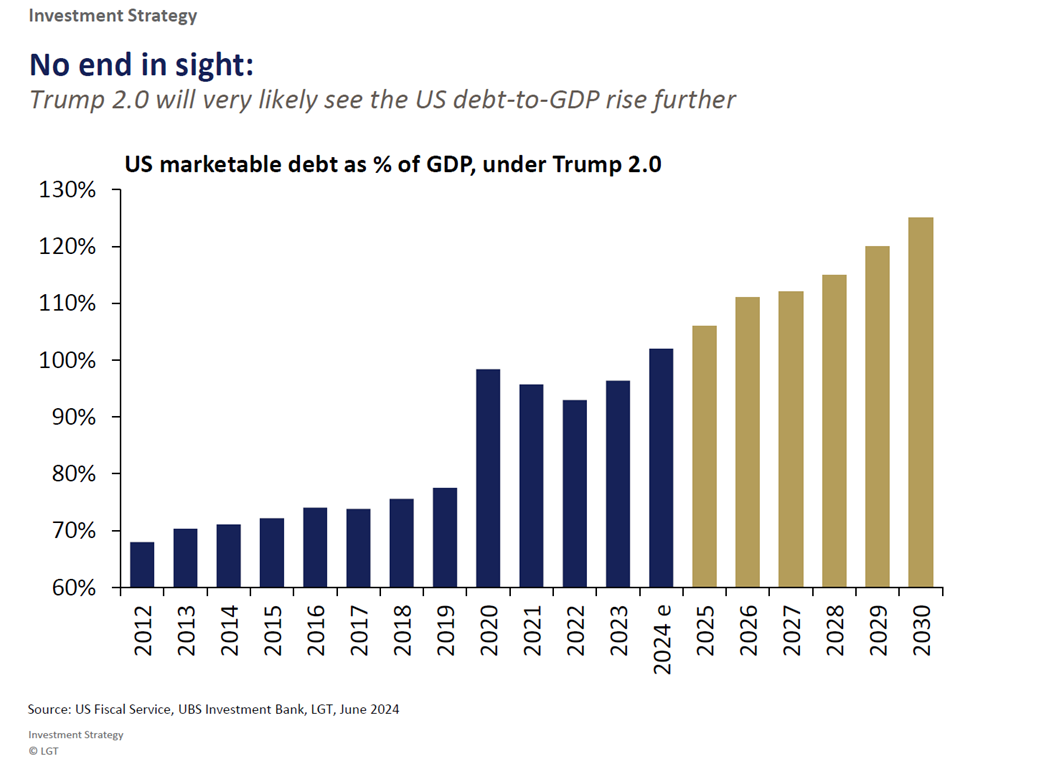

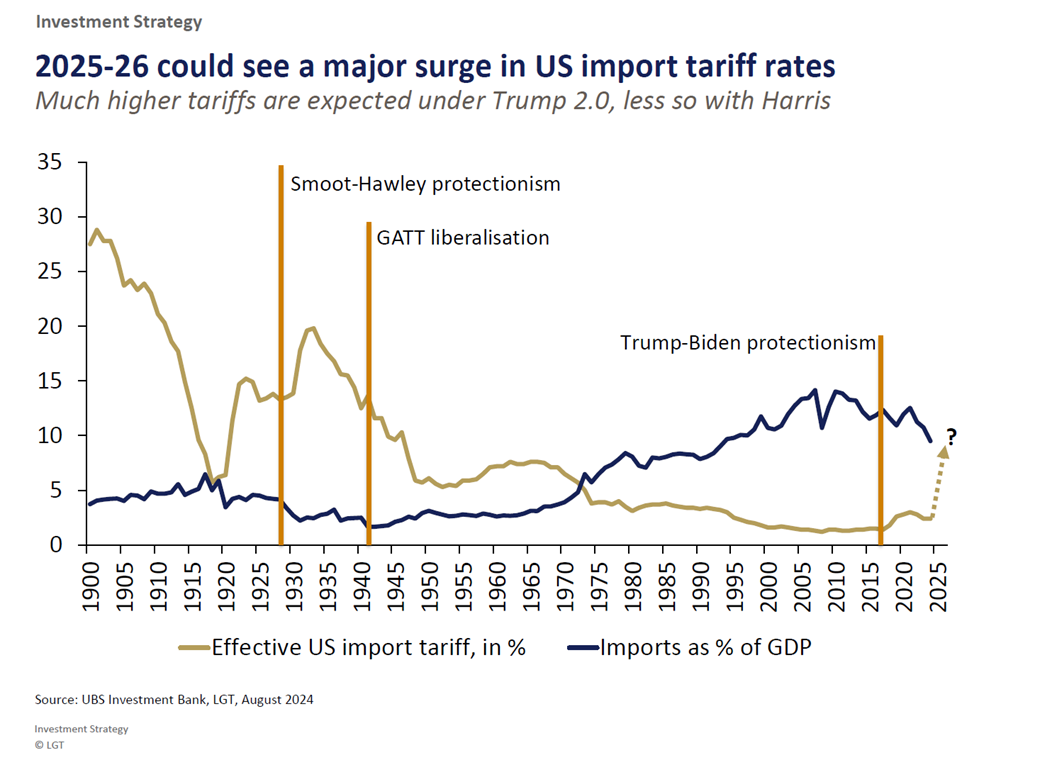

I came across a great chart deck this week, so let me summarise the key themes.

Post 2020 – it’s fairly clear that we’ve shifted into a fiscal dominance regime.

In simple English – this means get used to governments spending a lot more money, even if it means putting them in a budget deficit position.

Under Trump, this is not likely to change.

US debt to GDP ratio is likely to continue to rise.

At the same time, US is likely to run a more America first, protectionist policy – so be prepared for tariffs.

What does that all mean for a Singapore bank investor?

Well I suppose with a more resilient US economy, we’ll probably see a resilient Singapore economy as well.

And with higher long term interest rates + a steeper yield curve, that would definitely benefit bank stocks.

So you know what I completely get why bank stocks soared after the Trump win.

But as investors, you usually want to spend more time thinking about the risks than the bull case.

As long as you manage downside risk well, the upside will find a way to take care of itself.

I’ve noticed this in many years of investing, and it’s just so true.

As shared in the REITs article, my biggest fear in 2025 is for the potential return of inflation, and a rise in long term interest rates.

You can see how US 10 year yields have recently crept up to 4.77%.

In my view the 4.5 – 5.0% is the “danger zone” where each time long term yields went into this area the past 2 years, it coincided with a sell-off in stocks (this time being no different).

And yes I know that the recent US CPI data came in weak, which led to a relief rally across the board this week.

But as long term investors, you’re not really looking at the short term.

You want to zoom out and try to imagine how the world will look 18 months from now.

And with Trump running a large budget deficit, protectionist policies, and large fiscal spending – boy my biggest concern really is the return of inflation and higher long term interest rates.

For now, Singapore interest rates are relatively muted at 3.08%, but if they march up towards 3.5% – how would Singapore bank stocks react?

I overlaid Singapore 10 year yields (red) against DBS Bank below (candles).

And as you can see – actually there is no strong correlation between the two.

For most of 2023-2024 while Singapore 10 year yields bounced around from 2.8% – 3.5%, DBS Bank stock remained largely rangebound.

And it was only after the Nov elections when the outlook for the economy and yield curve changed materially, that we saw a huge step up in DBS Bank share price.

So in fact the key takeaway seems to be that the bigger underlying factor driving DBS’s share price is not long term interest rates – but the economic outlook, and the steepness of the yield curve.

So to put it simply.

I guess what I’m trying to say – is that you know what I could see Singapore bank stocks holding up pretty well even if long term interest rates march higher, as long as the economy remains resilient.

Follow Financial Horse to avoid missing any post!

But that’s just half the analysis.

The other half – is price (or valuations).

At latest price of 43.5, DBS Bank pays a 4.98% annualised dividend yield.

That’s about a 2% yield spread vs the latest 6-month T-Bill or 10 year government bond.

DBS Bank’s book value is 22.1, so the Price/Book ratio is 1.96x

Visualised below – you can see how this is the highest Price/Book DBS Bank has had since IPO.

Higher than even the 2007 highs.

To be absolutely fair to DBS Bank.

If you pull up the Price/Book ratio for the other Singapore banks, the chart couldn’t be more different.

Yes Price/Book for OCBC Bank is high, but nowhere near 2007 levels.

Likewise for UOB Bank

This suggests the record high valuations for DBS is unique to DBS – and not an industry wide overvaluation for Singapore banks.

It suggests that DBS is valued expensively today more due to the strong performance of DBS Bank (as illustrated by their 17.6% ROE), rather than an overvaluation of the entire banking sector.

If so, this is actually a good sign for DBS Bank.

Okay I know I brought up a lot of points above.

But at the end of the day, we need to have a conclusion.

Will I buy more DBS Bank stock at 5.0% dividend yield?

I can’t find the exact words that I used.

But at $38 I wrote that in the most optimistic macro scenario, I could see DBS Bank going into the 43 – 45 range.

And you know what – DBS Bank is at that price range today.

At this price, I really struggle to get comfortable with the risk-reward analysis.

How much further capital gains upside is possible at these levels?

And given that current price is pricing in a fairly optimistic macro outcome, any small wobble on the macro outlook and you could be looking at downside risk.

All while DBS has already announced a $3 billion share buyback plan, so some of that capital return would already be priced into the stock.

I think bottom line for me today.

Is that at $43, I do struggle to get comfortable with the risk-reward, given what looks to be priced into the stock today.

It just seems to me that I would be risking a lot of capital, for a small amount of upside here.

Just to be clear, I’m not saying that DBS Bank is a bad investment, as I completely get that the macro outlook under Trump is favourable for banks.

I just prefer to find investments where the risk-reward is somewhat more balanced, in that I am risking a small – moderate amount of capital for a large amount of upside.

See my full stock watchlist and personal portfolio on FH Premium if you are keen.

Personally I hold a position in OCBC Bank, so read into that what you will.

I find valuations for UOB Bank or OCBC more attractive, which helps to manage the downside risk somewhat.

But I also get that sometimes in investing – you just want to buy the market leader and be done with it, and it’s fairly clear that in this case DBS Bank is the market leader among Singapore banks.

So for those of you who own DBS Bank, trust me I understand why.

In any case, that’s how I’m seeing DBS Bank and the Singapore banks today.

But regular readers know that while I have my views, I have no problems to change my mind on a dime if and when facts change.

So do know that about me, and don’t be afraid to change your mind as well.

My latest macro views, including my full stock watchlist and personal portfolio, is shared on FH Premium.

This post is written on 16 Jan 2025 and will not be updated going forward. My latest views on markets, my Stock watchlist and full Personal Portfolio, are shared on FH Premium.

Fractional investing allows you to buy portions of expensive stocks like Google or Apple, and also allows you to add meaningful diversification to your portfolio even with smaller sums of capital.

You can own a share of the world’s biggest companies like META, NVDA and TSLA for just USD5.

Plus! Young investors (18 – 25 years old) can enjoy zero commission fees for your trades with the DBS Young Investor Account.

Find out more here.

A week or two back I shared my views on REITs in 2025. And I know a lot of you have been asking. So let me share my views on Singapore banks as well. I mean if you really think about it, on the SGX there’s really only REITs and Bank stocks to buy. So

The post Will I buy more DBS Bank stock at a 5.0% dividend yield? Are Singapore Bank stocks still a good buy? appeared first on Financial Horse.